By Keith Sampson, Senior Vice President, Energy Services

In his January 2023 blog titled “New England Energy Trends in 2023: What’s on Keith Sampson’s Mind,” Keith shared his viewpoint on energy market trends for 2023. With the first quarter of the year nearly complete – and with more information at hand – Keith shares a revised forecast for 2023 New England energy trends, including his thoughts on the impact of the Russia-Ukraine conflict – one year into the war that has singlehandedly changed the energy market across the world over the last year.

In your January Blog, titled “New England Energy Trends in 2023: What’s on Keith Sampson’s Mind,” inflation, supply chain, the impact of reduced natural gas and oil flowing from Russia, along with natural gas inventory levels was top of mind for you? What are you thinking about today with respect to these issues and what do our clients need to know as they progress through 2023?

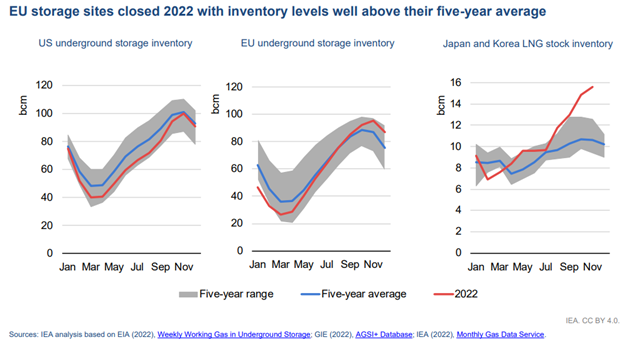

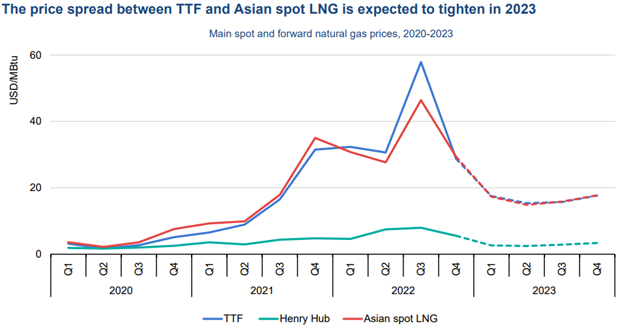

The big thing that’s happened since my January 2023 blog is that world LNG prices have continued to decline and are now at the same level they were prior to the Russian invasion of Ukraine. In addition, NYMEX Henry Hub natural gas futures have fallen from a high of $8 per MMBTU in the summer of 2022 to as low as $2.10 on February 17. What this means for consumers is a decline in natural gas and electricity futures. The primary driver behind these declines is the one thing we cannot forecast or predict, which is weather. Unseasonably warm temperatures in New England, North America, and Europe have resulted in inventory improvements.

Domestically, natural gas storage levels are slightly above the five-year average, resulting in the Henry Hub price falling. Internationally, Europe’s storage levels are at 80 percent of peak capacity with a few weeks of winter remaining, putting that region in an excellent position headed into the summer. Thus, causing a corresponding decline in the Dutch TTF, which we defined in my previous blog, “New England Energy Trends in 2023: What’s on Keith’s Mind.”

This trend was highlighted in the latest quarterly natural gas report from the International Energy Agency[1]:

(Figure 1) – International Energy Agency: European Union Storage Sites/Inventory Levels, based on U.S. Energy Information Administration (EIA) 2022

Figure 2: Price Spread Between TTF and Asian Spot LNG

So now is an important time for consumers to consider locking all or some of their future energy commodity contracts.

The energy markets have continued to fluctuate – and seemingly improve. Can you explain those opportunities along with any pitfalls you see for the year ahead? What should our clients be aware of?

Many Competitive Energy Services’ clients are taking advantage of these lower prices, allowing them to buy the dip. The question on everyone’s mind is “will the markets continue to decline further?”

Regarding natural gas, the Henry Hub natural gas futures are certainly in the bottom 10 percent of the decade low range. Something that typically happens when we’re in the bottom of the range is the market becomes contango, where prices are higher further into the future compared to near-term markets. This is the market’s way of saying it believes prices have a greater chance of increasing in the future.

While markets might see further moderate declines in the near term, there a number of bullish factors to consider. The Freeport LNG Export Terminal that has been offline since a fire that occurred on June 8, 2022, has just received approval to begin exporting again, which will put a strain on the already fragile natural gas supply and demand condition. Additional LNG export capacity is scheduled to occur starting in 2024 into 2025. This will add 25 percent additional LNG export demand that will need to be filled by domestic natural gas producers. As of this writing, the source and delivery infrastructure of that supply is not fully developed.

Recently, we just marked one year since the beginning of the Russia-Ukraine conflict. How is this ongoing war impacting energy pricing now and what can we expect in the near term?

From the start, Russia has weaponized energy commodities, especially natural gas. Russia energy sanctions continue to divert oil and natural gas away from traditional European destinations. To combat the situation, Europe has used ingenuity to develop alternative supply and delivery pathways. In addition, Europe was extremely lucky that the weather remained mild throughout this past winter. Thus, never truly testing the impact of a cold winter on the alternative approach to natural gas delivery and electricity generation.

This was a long of answering your question. Nothing has fundamentally changed since the beginning of the invasion and Europe continues to rely on LNG imports. That demand continues to put bearish pressure on world LNG prices, the same LNG that New England would have desperately needed had we had traditional cold winter weather, which leaves us all wondering and the market analyzing what is the statistical probability that New England and Europe will experience another above-average cold-weather season.

How has the U.S. position changed in the last year? What are the factors at play that are influencing energy costs in this country?

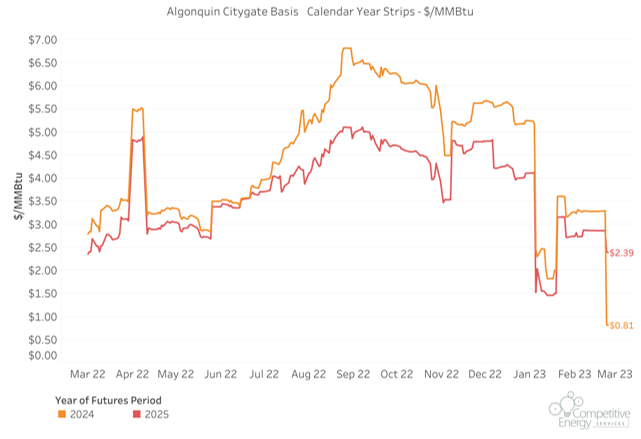

As mentioned earlier, NYMEX Henry Hub natural gas futures have fallen from a high of $8 per MMBTU in the summer of 2022 to as low as $2.10 on February 17, as a result of improved domestic natural gas inventory levels, as you can see in the graph below.

Figure 3 – Algonquin Citygate Basis Calendar Year Strip - $/MMBtu - Competitive Energy Services

Where are the shortfalls in the energy industry that will impact the supply?

- Russian exports and sanctions

- New England interstate natural gas supply infrastructure

- National electricity transmission to efficiently serve usage hubs with clean renewable energy

- Electrical infrastructure to support the needed move toward clean energy and electrification

The ban on Russian Distillate Products by the European Union and the European Russian Embargo is hard to ignore. How much Russian gas and oil is being produced and not being used? If Europe stops buying gas and oil from Russia, where are they getting it? And what will the rest of the world do?

Given this ban just went into effect in early February, it may be too early to fully understand the longer-term implications. That said, the ban is significant – last year, European countries met about half of their total diesel consumption through Russian imports. Given Europe has limited capacity to refine crude oil directly, refined products are expected to be imported from other sources - primarily from the Middle East, along with the U.S. and India. Meanwhile, it is expected that Russia will find other markets for refined products at a discounted price, and/or increase its crude oil sales to China and India which could then refine it. Over the past year, we have seen how this realignment of global energy flows can at first disrupt markets, before eventually rebalancing, albeit likely at a higher price point. While prices have already risen in Europe, and Russia will likely feel the impact of a much more limited market, ultimately if Russian products continue to make it into the global supply it will help limit scarcity and prevent price spikes.

What kind of strain is that putting on the U.S. in terms of meeting the demand?

The ban on Russian products has already impacted global prices for oil and distilled products, and the U.S. should continue to feel these ripple effects on the global market. Though, as a major crude oil producer with significant refining capacity, domestic supplies for distilled products are in a much better position than Europe. Markets appear to be settling a bit as we come out of a warm winter with supplies in relatively good shape, but there remains a great deal of uncertainty regarding the global economy and implications for prices this summer in preparation for next winter.

And what about New England’s reliance on LNG imports? How will that impact next fall and winter?

If it’s cold, it will have an impact and at some point, between now and next winter, when the market realizes that bearish situation is a reality, it’s highly probable that prices will increase and could increase throughout the summer into fall – until real winter conditions become a reality. This is a mirror image of the situation we were in 10 months ago.

[1] https://iea.blob.core.windows.net/assets/c6ca64dc-240d-4a7c-b327 e1799201b98f/GasMarketReportQ12023.pdf