To help keep our clients ahead of the curve when it comes to their energy initiatives, CES publishes a weekly market newsletter which discusses key energy events, provides market analysis, and delivers a practical summary of current market conditions.

The 12-month rolling strip for Brent was flat week-over-week at $84.61/barrel and increased for WTI by 1.9% week-over-week to $80.42/barrel. Lower crude oil prices are helping bring down spot gasoline prices. The NYMEX prompt month lost $0.06/MMBtu week-over-week to $3.23/MMBtu while the NYMEX rolling 12-month strip decreased by $0.01/MMBtu this week to $3.46/MMBtu. Storage levels saw a net increase of 95 Bcf for the week ending May 29th. The NEPOOL 12-month electricity strip gained 2.98% week-over-week to $81.72/MWh. The 2027, 2028, and 2029 strips all increased week-over-week.

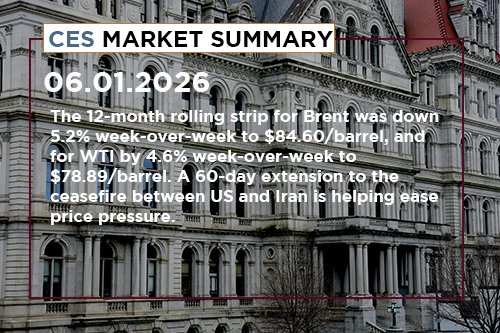

The 12-month rolling strip for Brent was down 5.2% week-over-week to $84.60/barrel, and for WTI by 4.6% week-over-week to $78.89/barrel. A 60-day extension to the ceasefire between US and Iran is helping ease price pressure. The NYMEX prompt month lost $0.38/MMBtu week-over-week to $3.29/MMBtu while the NYMEX rolling 12-month strip increased by $0.18/MMBtu this week to $3.47/MMBtu. Storage levels saw a net increase of 92 Bcf for the week ending May 22nd. The NEPOOL 12-month electricity strip gained 0.49% week-over-week to $79.36/MWh. The 2027, 2028, and 2029 strips all increased week-over-week.

The 12-month rolling strip for Brent was down 3.3% week-over-week to $89.28/barrel, and for WTI by 5.3% week-over-week to $82.69/barrel. Markets face renewed volatility after fresh U.S. strikes on Iran. The NYMEX prompt month lost $0.05/MMBtu week-over-week to $2.91/MMBtu while the NYMEX rolling 12-month strip decreased by $0.10/MMBtu this week to $3.29/MMBtu. Storage levels saw a net increase of 101 Bcf for the week ending May 15th. The NEPOOL 12-month electricity strip fell 2.77% week-over-week to $78.97/MWh. The 2027, 2028, and 2029 strips all decreased week-over-week.

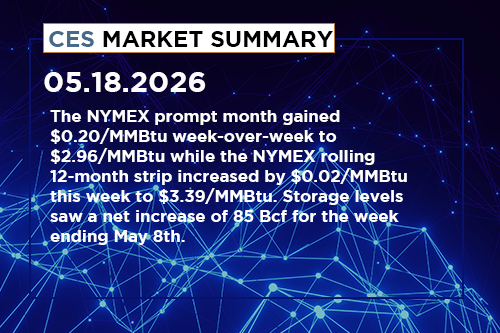

The 12-month rolling strip for Brent was up 4.8% week-over-week to $92.29/barrel, and for WTI by 6.4% week-over-week to $87.34/barrel. Global oil inventories are down as the Strait of Hormuz remains closed for shipping. The NYMEX prompt month gained $0.20/MMBtu week-over-week to $2.96/MMBtu while the NYMEX rolling 12-month strip increased by $0.02/MMBtu this week to $3.39/MMBtu. Storage levels saw a net increase of 85 Bcf for the week ending May 8th. The NEPOOL 12-month electricity strip rose 2.02% week-over-week to $81.22/MWh. The 2027, 2028, and 2029 strips all rose week-over-week.

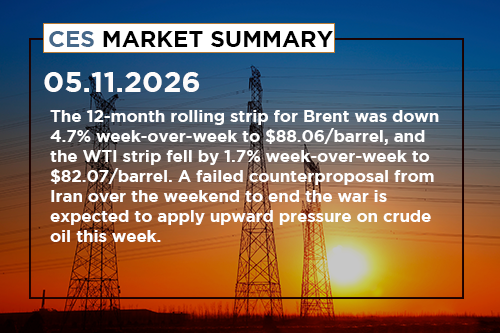

The 12-month rolling strip for Brent was down 4.7% week-over-week to $88.06/barrel, and the WTI strip fell by 1.7% week-over-week to $82.07/barrel. A failed counterproposal from Iran over the weekend to end the war is expected to apply upward pressure on crude oil this week. The NYMEX prompt month lost only $0.02/MMBtu week-over-week to $2.76/MMBtu while the NYMEX rolling 12-month strip decreased by $0.07/MMBtu this week to $3.37/MMBtu. Storage levels saw a net increase of 63 Bcf for the week ending May 1st. The NEPOOL 12-month electricity strip fell 1.74% week-over-week to $79.61/MWh. The 2027, 2028, and 2029 strips all fell week-over-week.

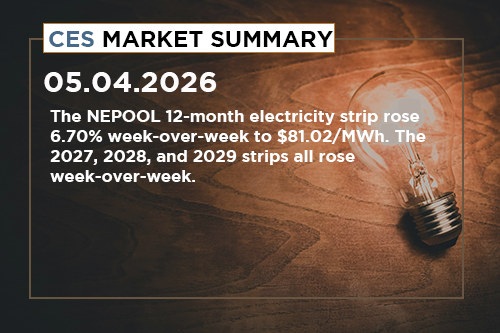

The 12-month rolling strip for Brent was up 5.1% week-over-week to $92.42/barrel, and for WTI by 4.1% week-over-week to $83.52/barrel. A long-rumored but sudden departure of the UAE from OPEC last Friday could shake up crude oil supply and market alliances in the future. The NYMEX prompt month gained $0.26/MMBtu week-over-week to $2.78/MMBtu while the NYMEX rolling 12-month strip increased by $0.09/MMBtu this week to $3.44/MMBtu. Storage levels saw a net increase of 79 Bcf for the week ending April 24th. The NEPOOL 12-month electricity strip rose 6.70% week-over-week to $81.02/MWh. The 2027, 2028, and 2029 strips all rose week-over-week.

The 12-month rolling strip for Brent climbed 9.5% week-over-week to $87.92/barrel, and WTI rose 6.2% week-over-week to $80.25/barrel. Prices in the U.S. are expected to rise this week over uncertainty on the next stage of peace talks in the conflict between the U.S. and Iran. The NYMEX prompt month fell $0.15/MMBtu week-over-week to $2.52/MMBtu while the NYMEX rolling 12-month strip decreased by $0.06/MMBtu week-over-week to $3.35/MMBtu. Storage levels saw a net increase of 103 Bcf for the week ending April 17th. The NEPOOL 12-month electricity strip rose 4.7% week-over-week to $75.93/MWh. The 2027, 2028, and 2029 strips all rose week-over-week.

The 12-month rolling strip for Brent was down 3.4% week-over-week to $80.26/barrel, and WTI fell by 5% week-over-week to $75.57/barrel. Gas prices in the US are expected to rise this week after escalations in the US-Iran conflict due to a US Navy blockade of Iranian vessels. The NYMEX prompt month gained $0.03/MMBtu week-over-week to $2.67/MMBtu while the NYMEX rolling 12-month strip decreased by $0.02/MMBtu week-over-week to $3.41/MMBtu. Storage levels saw a net increase of 59 Bcf for the week ending April 10th. The NEPOOL 12-month electricity strip fell 5.54% week-over-week to $72.56/MWh. The 2027 and 2028 strips fell week-over-week, while the 2029 strip rose slightly.

The 12-month rolling strip for Brent is down 1.2% week-over-week to $83.09/barrel, and the WTI strip is down 0.7% week-over-week to $79.55/barrel. After the failure of U.S.-Iran peace talks in Pakistan over the weekend, the U.S. is set to blockade the Strait of Hormuz starting today. The NYMEX prompt month dropped by $0.15/MMBtu week-over-week to $2.65/MMBtu while the NYMEX rolling 12-month strip decreased by $0.10/MMBtu week-over-week to $3.43/MMBtu. Storage levels saw a net increase of 50 Bcf for the week ending April 3rd. The NEPOOL 12-month electricity strip fell 2.26% week-over-week to $76.82/MWh. The 2027 strip fell slightly week-over-week, while the 2028 and 2029 strips rose slightly.

The 12-month rolling strip for Brent was down 6% week-over-week to $84.09/barrel, and for WTI it was down 1.9% week-over-week to $80.15/barrel. Intermediaries are working with U.S, Israel, and Iran on a ceasefire proposal as the US deadline to Iran for an opening of the Strait of Hormuz draws nearer. The NYMEX prompt month dropped by $0.20/MMBtu week-over-week to $2.80/MMBtu while the NYMEX rolling 12-month strip decreased by $0.16/MMBtu week-over-week to $3.53/MMBtu. Storage levels saw a net increase of 36 Bcf for the week ending March 27th. The NEPOOL 12-month electricity strip fell 2.17% week-over-week to $78.59/MWh. The 2027, 2028, and 2029 strips saw mixed movement week-over-week.

The 12-month strip for Brent is down 1.4% week-over-week to $90.45/barrel, and the 12-month strip for WTI is down 3.3% week-over-week to $82.42/barrel. US production of crude oil remains strong as global markets grapple with a major supply shock caused by the Iran conflict. The NYMEX prompt month remained at $3.10 week-over-week, while the NYMEX rolling 12-month strip decreased by $0.07/MMBtu week-over-week to $3.77/MMBtu. Storage levels saw a net withdrawal of 54 Bcf for the week ending March 20th. The NEPOOL 12-month electricity strip rose 5.78% week-over-week to $81.16/MWh. The 2027 and 2028 strips rose week-over-week while the 2029 strip decreased slightly.

As global oil supply continues to tighten, the Strait of Hormuz is drawing more military attention from both Iran and the US. The 12-month strip for Brent was up 5.7% week-over-week to $91.76/barrel, and the 12-month strip for WTI was up 2.3% week-over-week to $85.27/barrel. The NYMEX prompt month declined by $0.04/MMBtu week-over-week and is now trading at $3.10/MMBtu. The NYMEX rolling 12-month strip increased by $0.01/MMBtu week-over-week to $3.84/MMBtu. Storage levels saw a net increase of 35 Bcf for the week ending March 13th. The NEPOOL 12-month electricity strip fell 1.24% week-over-week to $76.73/MWh. The 2027 strip rose week-over-week while the 2028 and 2029 strips decreased slightly.

The ongoing conflict in the Gulf and a blockade of the Strait of Hormuz by Iran continue to apply dramatic upward pressure in the markets. The 12-month strip for Brent was up 11.4% week-over-week to $86.85/barrel, and the 12-month strip for WTI was up 11.1% week-over-week to $83.32/barrel. The NYMEX prompt month declined by $0.06/MMBtu week-over-week and is now trading at $3.13/MMBtu. The NYMEX rolling 12-month strip has a similar weekly drop of $0.08/MMBtu to $3.83/MMBtu. Storage levels saw a net withdrawal of 38 Bcf for the week ending March 6th. The NEPOOL 12-month electricity strip rose 1.05% week-over-week to $77.69/MWh. The 2027 and 2028 strips rose week-over-week while the 2029 strip decreased slightly.

Escalations in the Iran conflict have sent global oil markets into a buying frenzy. The 12-month strip for Brent was up 11.4% week-over-week to $77.94/barrel, and the 12-month strip for WTI was up 15.6% week-over-week to $75.03/barrel. The NYMEX prompt month rose by $0.33/MMBtu week-over-week and is now trading at $3.19/MMBtu. The NYMEX rolling 12-month strip has a similar weekly gain of $0.34/MMBtu to $3.92/MMBtu. Storage levels saw a net withdrawal of 132 Bcf for the week ending February 27th. The NEPOOL 12-month electricity strip rose 10.81% week-over-week to $76.88/MWh. The 2027 and 2028 strips rose week-over-week while the 2029 strip decreased slightly.

Sign up with your email address to receive news and updates about energy markets.