By Aaron Rubin, Senior Energy Analyst

Historical Policy Overview

In 2009, the Massachusetts Department of Energy Resources (MA DOER) passed the Alternative Energy Portfolio Standard (APS) to help support new energy systems in Massachusetts that increase efficiency and reduce the need for conventional fossil fuel generation. Similar to a Renewable Portfolio Standard, the APS incentivizes the adoption of qualified technologies by requiring competitive electricity providers serving load in Massachusetts to cover a fixed percentage of total electric load with Alternative Energy Certificates (AECs).[1] Owners of enrolled APS technologies generate the AECs that are sold to utilities to meet APS compliance obligations.[2] The sale of AECs helps produce the revenue required to fund the development of eligible APS technologies. The actual price received per AEC sold can vary according to supply and demand fundamentals. To date in the APS program, a majority percentage of total AEC generation has been produced by eligible natural gas-fired combined heat and power systems (CHPs).

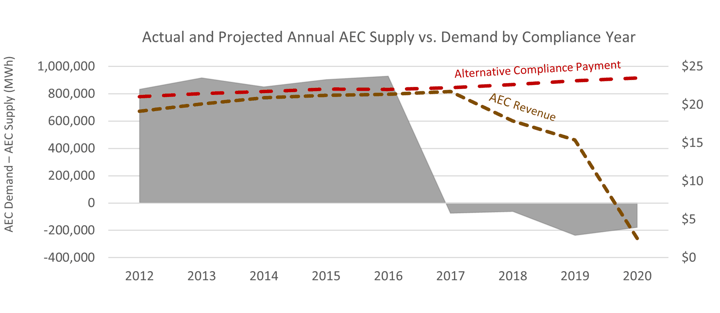

Beginning in 2018, the price of AECs plummeted as new CHP plants achieved commercial operation. As these new plants came online, the supply of AECs began to outstrip demand. Several eligible projects were built on the expectations that the sale of AECs from 2018 through 2021 would trend much closer to $20, a price level that is often viewed as the incentive level necessary to make new geothermal and other renewable thermal technologies economically viable. The significant decline in AEC prices, as shown in Figure 1, led the MA DOER to conduct a 2020 APS Review. This review outlined the reasons behind the fundamental supply and demand imbalance in the program. A key takeaway from the DOER’s study included that the APS would have a worsening supply and demand outlook if left unchanged, largely because CHP generation is expected to continue to produce the majority of future annual AEC supply.

Figure 1: The decline in AEC pricing in response to oversupply of AECs on the market beginning in 2017. The difference between annual AEC pricing and the annual alternative compliance payment is increasing. The MA DOER’s Straw Proposal attempts to address the oversupply of AECs.

APS Straw Proposal Review

In July 2021, the MA DOER released the APS Straw Proposal for stakeholder review. The proposal aims to guide AEC pricing back to historical levels exceeding $20/MWh by addressing the oversupply of AECs currently on the market. Under the Straw Proposal, the APS compliance obligation will increase by 2% in 2023, expanding the total percentage of utility loads required to be covered with the purchase of AECs. In addition to increasing demand for AECs, the Straw Proposal will also phase CHP systems out from the APS program using a declining percent multiplier of total AEC production previously available from CHP units. This multiplier will start at 70% in 2023 and then decline by 10% annually until CHPs are removed from the program entirely by 2030. As depicted in the graph below, the removal of CHPs from the program will reduce AEC supply on the market at the same time as demand for AECs increases under the newly proposed and higher utility compliance obligation requirement.[3] With AEC supply at a shortage to AEC demand, prices are anticipated to rise back near or above historical price levels. The intended effects of the Straw Proposal are illustrated in Figure 2.

Figure 2: AEC pricing will increase in 2023 in response to the supply and demand adjustments outlined in the APS Straw Proposal.

Straw Proposal Repercussions and Opportunities

If the Straw Proposal is enacted as written, CHPs enrolled through the APS will sell fewer AECs beginning in 2023 but are likely to receive a higher price from each AEC sale. As a result, in 2023, APS revenues for enrolled CHP systems under the Straw Proposal may actually increase year-over-year as added revenue from the growth in the value per AEC outstrips the decline in CHP AEC production (reduced by just 30% from the current credit calculation baseline). This higher AEC revenue, however, would be just a short-term benefit, as the complete phase-out of CHPs from the APS program by 2030 eventually limits the quantity of future AEC sales to zero.

The intent of DOER’s removal of CHPs from the legislation is to provide financial assistance for remaining eligible program technologies. As noted above, AEC prices are likely to return to prior higher levels. As a result, the Straw Proposal provides an opportunity for enrolling new qualifying program technologies that are pre-existing or planned for development. Additionally, high multipliers to the base incentive rate exist for various renewable thermal technologies including solar hot water systems, air-source heat pumps, and geothermal heat pumps. For the list of eligible program technologies and list of renewable thermal multipliers, please access the qualification application on the DOER’S APS webpage.

CES has assisted many of our clients with modeling the impacts of MA DOER incentive programs, enrolling qualified technologies in the APS program, and selling AECs in the marketplace. If you are interested in learning more about how changes to the APS outlined in the Straw proposal could provide opportunities for your business, please reach out to a member of our Energy Services team for further discussion.

[1] Currently, eligible Massachusetts APS projects include combined heat and power systems (CHPs), fuel cells, waste-to-energy systems, and renewable thermal technologies (air-source heat pumps, ground-source heat pumps, and solar thermal). When the APS was initially established, 1.5% of state utility loads had to be met with APS eligible technologies. Under current regulations, this requirement has increased by 0.25% annually.

[2] The current APS policy enables owners of enrolled technologies to generate AECs for each megawatt-hour equivalent of alternative thermal and electrical energy that is produced relative to the fuel that is input.

[3] Pricing for 2023 through 2030 is estimated conservatively at $20 per MWh under the Straw Proposal. Incentive value could be closer to the newly proposed alternative compliance payment price depending on the amount of newly enrolled technologies that enter the program and produce AECs.

Photo by: Nuno Marques