By Andrew Price, President & COO

Hydrogen is getting a lot of attention these days, and for some very good reasons. In the U.S. and Europe, hydrogen markets are poised for rapid expansion due to several factors:

· Incentives: In the U.S. the 2021 Infrastructure and Investment and Jobs Act (IIJA) contained more than $9 billion in incentives for hydrogen – mostly targeted at creating multiple regional hydrogen manufacturing hubs. The 2022 Inflation Reduction Act (IRA) made more money available, establishing significant new production incentives for manufacturers of hydrogen. The IRA production incentives are on a sliding carbon scale – with the highest rates available to production methods that have the lowest carbon emissions. The European Union is also offering billions in incentives to promote hydrogen projects.

· Technology: While the use of hydrogen does not directly cause greenhouse gas (GHG) emissions, the production and handling of hydrogen can be GHG intensive. The increasing availability of low-cost wind and solar generation unlocks a zero-carbon pathway to manufacture hydrogen. Using zero carbon electricity and an electrolyzer to extract “green hydrogen” from water produces zero GHG emissions. So called “blue hydrogen” – hydrogen produced traditionally from natural gas, but with the carbon captured and sequestered underground – is also supported under the IIJA and IRA. Blue hydrogen is the focus of several of the manufacturing hubs proposed in response to the ongoing IIJA hydrogen hub competition.

· Demand: About 10 million metric tons of hydrogen is already produced in the U.S. each year, primarily for use in oil refining and ammonia production. Currently, most hydrogen is made from natural gas through a process that emits significant quantities of carbon dioxide. Reducing emissions associated with current hydrogen production is a near term focus of U.S. incentives and would be significant in the fight against climate change. To convert the total current demand level of 10 million metric tons to renewable electricity using electrolysis would require roughly 300 GW of solar, roughly 2 times the total installed solar capacity in the country today, or 150 GW of wind generation, essentially 100% of all wind generation currently installed in the U.S.

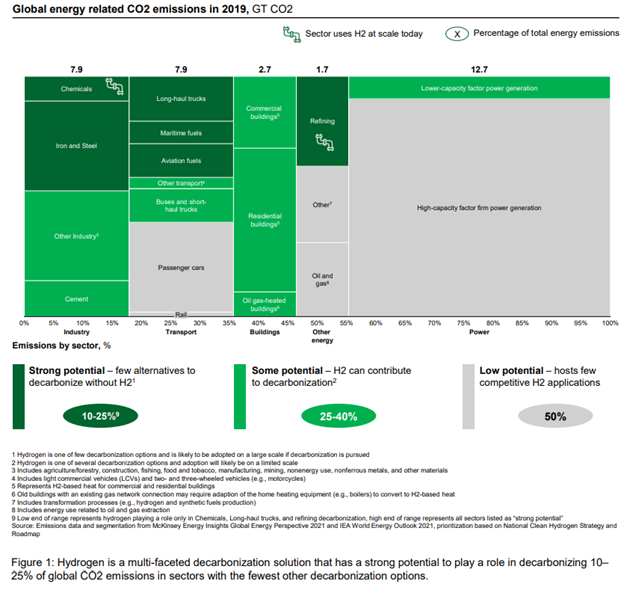

Hydrogen advocates envision many new use cases beyond the existing refining, chemical and fertilizer industries. Hydrogen is viewed as a viable future replacement for fossil fuels in industrial processes that are difficult to electrify (iron and steel, cement and certain other high temperature industrial applications). Using low or zero carbon hydrogen in these applications could help decarbonize up to a quarter of global energy-related CO2 emission according to a recently published Department of Energy (DOE) report.[1] The DOE identified economic sectors with the most potential to utilize low or zero carbon hydrogen. Collectively these sectors, shown in dark green in the following figure, represent 10% to 25% of global GHG emissions.

U.S. federal incentive programs are still being established but pilot hydrogen projects are already popping up across the US. The best uses for hydrogen in a zero-carbon future, however, is a topic of much debate. Hydrogen molecules act differently than natural gas molecules, and it is challenging to blend hydrogen in traditional natural gas pipelines above 20% by volume without modifications to older distribution systems and end use equipment. Hydrogen itself has been linked to increased greenhouse gases in the atmosphere.[2] To be viable, the clean hydrogen industry will need to avoid the leakage problems that have plagued the natural gas industry as systems are established to manufacture, store, ship and use hydrogen around the globe.

Cost is another significant factor in the adoption of lower carbon hydrogen. The high upfront cost of electrolyzers – the equipment used to turn water and electricity into hydrogen – means that it is relatively expensive to manufacture hydrogen today. This is especially true if expensive electrolyzers operate only during periods of excess wind/solar generation. Hydrogen can be manufactured when wind and solar generation is very high and stored for future use – an application that becomes interesting in the future when we will get most of our electricity generation from intermittent renewables and need flexible loads to soak up “excess” generation. Using expensive electrolyzers at low utilization rates would lead to even higher costs per unit of hydrogen produced.

Of course, this is exactly why governments are heavily incentivizing hydrogen projects. The U.S. and Europe want to drive down the cost to manufacture hydrogen – hopefully putting electrolyzer technology on a similar learning curve as wind, solar, and batteries – each of which realized dramatic 90% cost reductions as they achieved economies of scale over the past several decades.

In certain applications, green hydrogen may always struggle to compete with the direct use of renewable electricity. The process of converting green electricity to hydrogen and then converting the green hydrogen to heat will always have a much lower efficiency than using the electricity directly in air source or ground source heat pumps. For this reason, the direct electrification of most heating, cooling, and transportation systems is still the most viable path to deep decarbonization.

There are many applications, however, that won’t be easily electrified. Heavy industrial processes including the manufacture of steel and concrete, for example. Iron and steel production is estimated to account for as much as 9% of global GHG emissions with concrete production contributing about 8%.[3] Many of the technologies being explored to produce “green” steel and cement involve the use of hydrogen. Using hydrogen (or ammonia which can be produced from nitrogen and hydrogen) as fuel for air, ship, and perhaps truck travel is another sector receiving attention.

Companies interested in the production and use of hydrogen are waiting for the U.S. Treasury Department to clarify rules and regulations around how the carbon intensity of hydrogen will be measured. Section 45V of the IRA offers either an upfront investment tax credit (ITC) or an ongoing production tax credit (PTC) option. Incentives under both the ITC and the PTC will be on a sliding scale based on lifecycle GHG emissions. The maximum incentive offered under the IRA will be given to zero carbon hydrogen production methods with a 30% upfront investment tax credit or a $3/kg ($25 per million btu) production tax credit available over 10 years. For comparison, current production costs for green hydrogen are in the $5 to $8 per kg ($42 to $67 per million btu) range today, with traditional “grey” hydrogen, produced from natural gas (without carbon sequestration), around $1.50-$2 per kg ($12-17 per million btu).

To qualify for the maximum ITC/PTC incentive available under the IRA, prospective hydrogen manufacturers are looking for cost effective renewable electricity. It will be important for these companies to understand what requirements, if any, the Treasury will impose on the renewable electricity sources used to manufacture hydrogen in its lifecycle analysis. Until Treasury establishes clear guidance – expected as soon as April 2023 - it will be difficult for prospective manufacturing facilities to accurately value tax credits available under the IRA.

Thanks to the massive tailwind provided by federal incentives, hydrogen is poised for significant growth over the next decade. Low carbon and zero carbon options are likely to become more cost competitive with traditional fossil fuel production methods - thanks to the federal incentives included in the IIJA and IRA. As lower costs are achieved, blue hydrogen (hydrogen produced from natural gas with carbon capture) and green hydrogen (hydrogen produced from renewable electricity) will become more viable in a variety of applications. Replacing current carbon intensive production methods and unlocking greener options for the most difficult to decarbonize sectors of the economy - including heavy industrial and long-haul transportation -are the most obvious uses today.

For most consumers the growing green hydrogen sector is one to watch but will provide limited opportunities in the near term. Heavy industrials should pay closer attention as low- and zero- carbon hydrogen becomes more available and more competitively priced in the coming years.

[1] US Department of Energy Pathways to Commercial Liftoff: Clean Hydrogen, March 2023.

[2] Hydrogen itself is not a direct greenhouse gas. But once in the atmosphere, fugitive hydrogen can increase the global warming potential of other greenhouse gases significantly. See, for example: Atmospheric implications of increased Hydrogen use, April 2022: shorturl.at/adrD7

[3] Iron & Steel: https://worldsteel.org/publications/policy-papers/climate-change-policy-paper/

Concreate: https://www.nature.com/articles/d41586-021-02612-5

Photo by Anthony Rampersad