By Max Webb, Managing Director of Pricing and Zack Hallock, Senior Energy Services Advisor

It’s that time of year again when fall’s arrival, colorful landscape, and cooler temps has everyone thinking about the upcoming winter season. With that in mind, Senior Energy Services Advisor, Zack Hallock, and Managing Director of Pricing Analytics, Max Webb, are back again to discuss the upcoming winter weather forecast and its potential impacts on energy in the U.S. and abroad. In a recent conversation in the CES Portland office, Zack and Max talked weather, the national and global energy market, external factors and influences at play, and the resulting impact on energy prices.

Max: It seems like yesterday that we were writing our blog on last winter’s weather forecast. I recall our lengthy discussion on El Niño vs. La Niña. Zack – could you remind us of what those weather patterns mean and why it matters to us here in New England?

Zack: I would be happy to give a quick refresher, Max, and will start by saying this year’s weather prediction is not a straightforward “one or the other” scenario and more a shift along the spectrum of what type of winter we will have in both North America and inclinations of European outlook. That spectrum, which is really a recurring climate phenomenon, the El Niño-Southern Oscillation, or ENSO. The pattern can be recognized well ahead of the shoulder months by evaluating Pacific Ocean surface temperature deviations from the norm. This observable pattern in the Pacific Ocean impacts the strength and variability of both the Pacific and Polar Jet Streams. This impact on the jet streams, which drive seasonal variability, is important because it typically results in an effect on the Arctic based polar vortex. The polar vortex is key in winter outlooks because a fragmented polar vortex can have catastrophic effects on whichever part of the world it drops into. ENSO does truly have three phases along the spectrum, two of which are commonly discussed: “El Niño” and “La Niña.” The third phase of ENSO is a “Neutral” phase, but this phase does not persist like “El Niño” and “La Niña” typically do. This ENSO pattern shifts back and forth semi-regularly every three-to-five-years and each phase triggers predictable disruptions of temperature and precipitation. I would describe the variability of winters in North America and Europe as a symptom of this ENSO feature.

Max: What are the Pacific Ocean temperatures telling us right now about the upcoming winter?

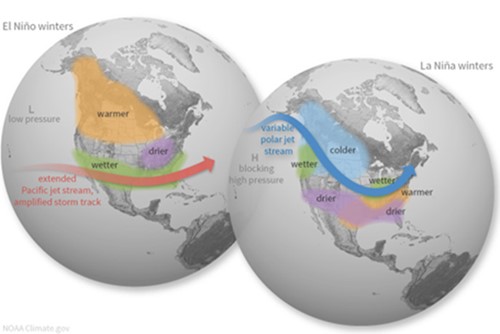

Zack: You could consider this winter an anomaly due to the fact this is a clear La Niña winter for the third winter in a row, dubbed “a triple dip La Niña.” We have had a triple dip La Niña before, but only five or six times since the 1950s, so not a lot to draw conclusions from in history. As these changes upset the large-scale air movements in the tropics, this effect can impact the strength and variability of both seasonal drought conditions in the Western U.S., as well as average precipitation all the way over in Europe. The maps below represent a typical El Niño vs. La Niña pattern on a North American winter highlighting the colder and wet pacific northwest and drier southern half of the continent.

Figure 1: El Niño and La Niña: North American ENSO Impacts

Max: It sounds like 2022-23 winter may play out in a similar way as the past couple of winters. Is there anything unique about our upcoming winter?

Zack: I’ll give you a classic “No and Yes” answer. Let me unpack that a bit. No, in the sense that both European and North American models are consistently predicting the same results from the current ENSO features, which means we are expecting a similar winter to last year. As with any La Niña winter, the new England region will average warmer than usual for the whole winter period, but the opportunity for swift cold intrusions (due to a fragmented polar vortex) is clear and present. Where we experienced a cold snap in January 2022, the current prediction is for a similar cold snap in December 2022. However, I am a bit skeptical on that timetable and would be bold enough to push that back to January 2023.

To address the “Yes,” one unique aspect about this coming winter goes back to January 2022, with the eruption of the submarine Hunga Tonga volcano in the south pacific. This event went largely under the radar in the United States, but it was one of the largest submarine eruptions since Pinatubo in 1991, which did have a measurable multi-year cooling effect around the globe. The Hunga Tonga eruption is significant for this year because of the amount of water vapor and sulfur emitted from just a single event. The stratosphere across the southern hemisphere saw a 10% increase in water vapor from just a single event, which for global climate terms is wildly immense. A change like this increasing stratospheric albedo causes less solar radiation to hit the planet’s surface, which in turn reduces the ability for the southern hemisphere to warm up. During the North American winter, the southern hemisphere should be in summer warming so the inability to warm as it typically does leads to a logical drop in average global temperatures. I am not saying this scenario will absolutely impact our winter in New England, but anytime you see anomalies like this you must keep the card in hand. I am honestly more curious to see how this will impact the ongoing conflict in Europe because, frankly, we all know what history says about prolonged winter conflict in Europe—nobody wins, and everyone freezes.

Max: Much of the news cycle continues to be dominated by the on-going war between Russia and Ukraine. I keep seeing headlines around Nord Stream and natural gas concerns for Europe this coming winter. Can you explain the connection?

Zack: Yes, at the end of the day this can be boiled down simply to a supply and demand imbalance that will reach a breaking point when the temperatures plummet in Europe. It is more a matter of when, not a matter of “if.” Nord Stream 1 is a predominantly underwater pipeline that goes from Russia to Germany through the Baltic Sea. There are several pipelines supplying Europe from Russia, but this major pipe is a symbol for Russia’s actions in their weaponization of a commodity. Up until the conflict, Russia accounted for ~30% of all natural gas supply to Europe through these pipelines. Now with the conflict in full swing, Russia is using natural gas supply as a weapon to gain leverage on the European Union and the United States. It is true that several countries in Europe – mainly Germany – are already telling citizens that there will be rationing efforts or even price caps this winter to ensure that critical infrastructure does not fail. Concerns have eased up a bit in Europe this month, but that first cold snap this fall will swiftly remind the world how precarious the supply situation is. The problem is that if Europe burns through their storage inventories too quick this winter, then they will be in the worst position imaginable as they continue to negotiate with Russia on a resolution.

Figure 2: Map of Underwater Nord Stream 1 Pipeline

Max: If Europe needs natural gas to generate electricity through this winter, and they are essentially cut off from Russian supply. From where are they getting the natural gas?

Zack: Now that Russia has cut off a large portion of Europe’s natural gas supply, Europe has turned to international supply sources to fill the void. Europe has historically received natural gas imports from Norway, North Africa, and other nearby countries, however, a newer source to the mix is U.S. imports of liquified natural gas (LNG). The U.S. has continued to increase its ability to ship liquified natural gas around the globe. According to the EIA, the U.S. has more LNG export capacity and has exported more LNG than any other country. The U.S. is expected to expand its LNG export capacity even further with additional export facilities approved and under construction. U.S. LNG imports have overtaken Russian natural gas supply to Europe since they have curtailed natural gas exports via the Nord Stream pipeline. With additional LNG export facilities on the way, I would expect the U.S. to continue to deliver more LNG to Europe as well as other countries who begin to rely more on natural gas as a primary fuel source.

Max: New England also relies on LNG as a backup fuel source throughout the winter on the coldest days, so I can imagine a scenario where the U.S. and Europe both need LNG shipments during a cold snap. What impact would that have on energy prices?

Zack: It sounds like you may already know where this is headed. As many of our clients and end-users in New England are aware, energy prices have been steadily increasing over the last year. The increased global demand for LNG is one of the main drivers behind that rise.

With uncertainty around their fuel sources for generating heat and electricity for the upcoming winter, Europe has been buying and injecting a ton of U.S. LNG into their storage facilities to use throughout the winter. Back in the U.S., New England’s primary fuel source for electricity generation is also natural gas. The northeast usually turns to LNG as a backstop to help boost generators on the coldest days of the winter. In effect, New England and Europe are bidding on the same LNG shipments. We may run into a scenario this winter when both countries are experiencing a cold snap and need all hands – or generators – operational to keep us warm and the lights on. If/When that happens, prices would likely spike on both sides of the pond.

On a positive note, according to Reuters, European natural gas storage is now at 92%, which exceeds their target of 80% to meet high demand during the winter. Since they’ve exceeded their storage goal, we have seen some pull-back in the global price for natural gas, which in turn, has resulted in some price relief here in New England.

The European benchmark for natural gas prices is the Dutch TTF Index. The TTF price will be important to monitor in the coming months as that price will be a key indicator on the direction of northeast natural gas basis and spot electricity pricing this winter.

Max: So not only do we need to keep an eye on our own back yard in terms of winter weather, but we should also be keeping an eye on European weather forecasts in case of cold weather. How do you expect the winter to play out for our European friends?

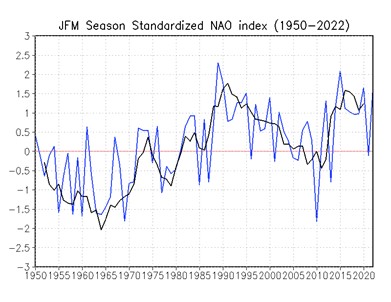

Zack: Agreed. In my opinion, New Englanders should pay attention to Europe’s weather this year – more so than any other winter to date – given this new global LNG landscape and the direct correlation to New England energy rates. Back to the overarching themes in North America due to ENSO, there are similar themes for Europe based on a consistent pressure feature called the “North Atlantic Oscillation” or (NAO). The NAO is characterized by a gradient of lower pressure farther north by Iceland up to higher pressure around the equator. The gradient and scale of that pressure difference between the “Icelandic Low” and the “Azores High” drives the strength and variability of westerly airflow across the Atlantic to Europe. When this pressure delta is large, it is considered a “positive” NAO and these westerly winds tend to be stronger and frequent northern Europe. When the gradient is minimal, it is considered a negative NAO, which means the strong winds frequent southern Europe instead of being directed north. The National Oceanic and Atmospheric Administration (NOAA) has been tracking the NAO since the 1950s and we have seen a persistent positive NAO for several years now indicating seasonal temperatures will remain elevated on average.

Figure 3: NOAA observation of NAO index during winter season

Interestingly enough, the call for winter in northern and even western Europe is very similar to New England; generally mild on average but when the cold comes, it will come with a fury to make up for the above average trendline. I will say the NAO feature is a fickle beast that often causes disagreement between the European model and the North American weather models partly because fluctuations can happen on a variety of timetables. Some changes can happen in a matter of days, whereas some fluctuations take months to develop, and the models typically disagree on this exact component of forecasting. This NAO feature is something we did not focus a lot on last winter but given the developing price relationship between Europe and New England, we need to have our ear to the ground in anticipation of foreign markets causing price volatility here in New England.

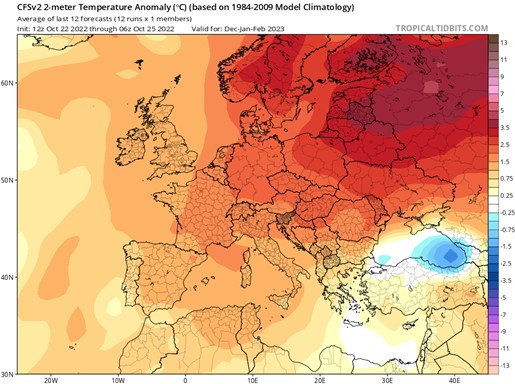

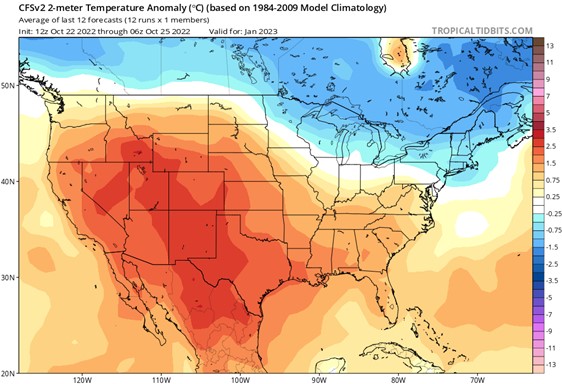

Figure 4: CFSv2 Climate Model for European Dec -Feb Average Temperature deviations (°C)

Max: Now that we have covered our bases from the Pacific to New England, all the way to Europe, let’s bring it home. What should we expect this winter in New England? I’m hoping for 70s and sunny….

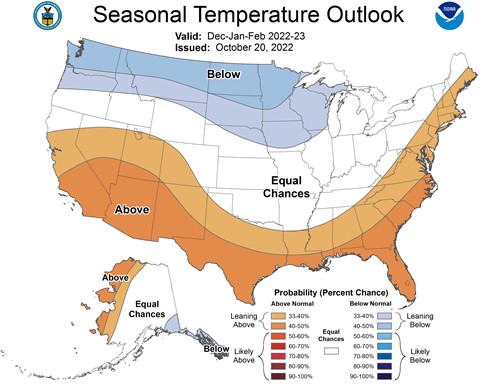

Zack: Maybe if you’re in Florida you will get that but, overall, it will “feel” warm for the most part this winter – similar to last winter, at least up until January 2023. The current prediction given all of the factors in play for this winter is an above average December 2022 - February 2023 period. However, to date the December 2022 period is flagged as the likely cold anomaly. I will mention here that December 2021 was slated to be the coldest month of the 2021-22 winter stretch. Instead, it held off until January 2022. This year, I would be comfortable making the claim that we will see a similar delay, with the cold snap occurring in January 2023.

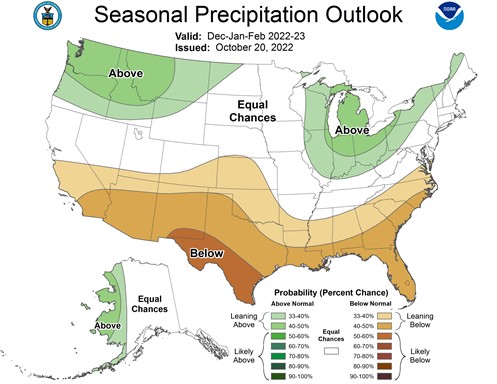

Figure 5: NOAA Dec- Feb Seasonal Temperature Outlook

Figure 6: CFSv2 Climate Model for January 2023 Average Temperature Deviations

For Europe, it would be fair to make a similar claim in that the northern and western regions of Europe will remain above average, but still harbor the opportunity to swing very cold very quickly. Both the severity and time aspect of these seasonal changes are key to anticipating reactions in the New England energy marketplace.

From a precipitation/ snow perspective, New England is slated to be slightly above average. Similar to New England, Europe is predicted to follow the same or very similar weather pattern. As an aside, this is where my professional and personal interests collide. The skier in me ideally hopes for record snow, but realistically, that isn’t likely to happen. Still, I will hope for a snowy surprise!

Max: Anything more from a precipitation outlook? I am sure a lot of snow enthusiasts are curious to hear the best time to hit the slopes this year.

Zack: Have you ever heard the phrase “No friends on a powder day?” All joking aside, it will likely be a tough start to the winter for outdoor enthusiasts in my opinion, much like last year. The New England region likely will not sustain adequate sub-freezing temperatures for low altitudes to retain an excess of snow accumulation. We may get a symbolic start to winter in December, but for something of great impact I am holding out for January. That said, I am optimistic, but I think most skiers with an understanding of the larger forces at play will massage the outlook until we have convinced ourselves this winter will be epic.

Figure 7: NOAA Dec- Feb Seasonal Precipitation Outlook

Max: To summarize our discussion today, this winter should play out very similarly to last year –relatively warm except for a couple-week stint in January and a few cold snaps here and there. Our European counterparts are in for a winter like ours with an expected above average temperature outlook with a few cold intrusions throughout. From an energy perspective, it sounds like we may be in for a wild few months depending on when those cold fronts make their way into the New England and into Europe. If they line up for some sort of perfect storm, we may see prices soar domestically. Those end-users with open positions or exposure to the spot market should expect to see higher than normal bills in some months depending on U.S. and European weather. Did I leave anything out?

Zack: With respect to energy, you are absolutely right that those with open positions, by design, enjoyed a moment of relief in October (following an unstable, high-priced summer) but anticipate continued volatility and elevated rates throughout the winter. Any winter month where the market does not go haywire is a blessing. Looking beyond this winter, my recommendation to everyone is to have an all-encompassing plan in place that allows for swift action when the opportunity to lock discounted rates presents itself over the next six-to-eight months. As the global LNG market stands, New England may have to endure this European influence beyond winter 2022-23. In summary, this winter looks like it will be very similar to last year in that we will have a delayed start to winter followed by a swift cold intrusion in the late December to mid-January period. The second half of the winter is always a toss-up after January, so I will save that for our mid-winter update.

Max: As an energy advisor, what is your recommendation for CES clients or anyone reading this blog as we head into this winter and beyond? Where does this leave a business during this volatile and unpredictable time? What can they expect or think about? How can they plan for the short- and long-term as they plan their current and future budgets, whether new to energy planning and management, or seasoned energy managers?

As an energy advisor, my guidance and advice are consistent. Facing this unpredictable time starts with having a thoughtful strategy to tackle individual priorities. Whether it is managing a short-term rate increase on your current budget or looking to average out increases over a longer period, businesses need to know market fundamentals driving this decision process. Opportunities currently exist – for example, outer year futures trade at a discount to the current market. For some this is a viable opportunity to mitigate risk while for others it simply does not make sense. Anticipating the arrival of opportunity or setting a “strike price” is just as important as mastering the current markets. This sets expectations with decisionmakers, so all parties have a realistic vision of the desired outcome and understand those impacts. Remember, in less than two years we have gone from one of the cheapest energy markets to one of the most expensive in our collective lifetime, so most are tackling an uncomfortable situation. Do not be afraid to leverage market volatility in your favor by taking a diversified approach that may be outside what you have done for the last 5-10 years.

At the end of the day, businesses should consider seeking objective advice. It is as simple as that. Energy markets and weather in particular can be unpredictable, but Competitive Energy Services’ guidance and perspective has been tried and true for almost 23 years now. Simply put, CES enables clients to achieve their energy and sustainability goals. This has been our purpose and our reason for being in business all of these years. If you are unclear or unsure about your particular energy woes, do not hesitate to seek that objective advice. CES continuously provides a pragmatic approach to help current and future customers navigate difficult times. Reach out to any CES Energy Services Advisor to discuss your company’s energy strategy, position, and options.

Painting of Portland Head Light, titled "Winter's Rage," by Helen Booth