By Lakshya, Bharadwaj, Senior Energy Analyst

On July 4, 2025, President Trump signed into law a budget reconciliation bill championed by Republicans and branded the One Big Beautiful Bill Act (OBBBA). While there is a long list of measures in the act that will have tangible and transformative impacts on public policy in the country, this blog will focus solely on what this piece of legislation means for the energy landscape.

In extending provisions of the Tax Cuts and Jobs Act (TCJA) of 2017, the OBBBA commits to a higher federal spending-to-revenue ratio and seeks to recoup some of the lost revenue by reducing green energy incentives. To do this, the OBBBA, as one of its key features, alters or removes many energy-related tax provisions introduced and implemented by the Inflation Reduction Act (IRA) of 2022, the last piece of federal mega-legislation with major ramifications for the energy sector.

While the policy restricts tax benefits previously granted by the IRA to renewable energy technologies such as wind and solar generation, it reverses some restrictions on the development of oil and gas in the United States. Industry giants, mid-tier and small-tier businesses, energy investment firms, and individual household units are all expected to be effected by the Act. The tax implications will likely permeate through many layers of business and everyday life, ranging from long-term capital and project planning to individual consumer decisions regarding whether to purchase an electric vehicle or install a heat pump.

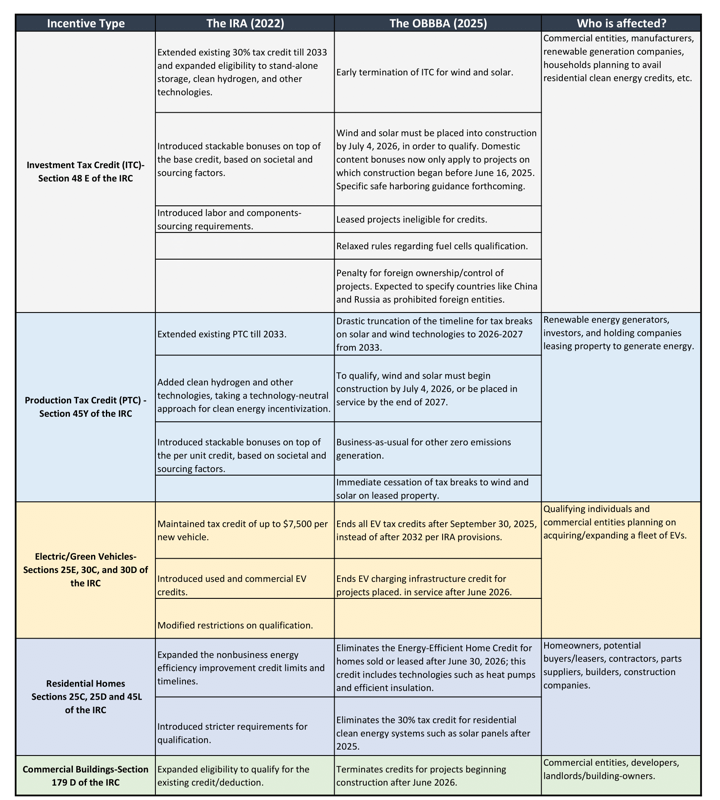

The IRA vs. The OBBBA: A Non-exhaustive Comparison

An attempt at breaking down the energy-related impacts of OBBBA without contextualizing it against the backdrop of the IRA might be a futile exercise. Hence, the matrix below touches upon some key points of comparison and provides an overview of the effected stakeholders. While not all-inclusive, this list of incentives covers the direct implications for many of the projects considered by CES clients.

The IRA also made it possible for nonprofit, municipal, and other non-taxpayer entities to benefit directly from tax breaks through direct pay, and the OBBBA maintains this mechanism. This means that while nonprofits, municipalities, and other non-taxpaying entities may still need to worry about rushing the timelines of planned projects or EV infrastructure, there is no imminent threat to the payment of tax benefits from those projects.

Measuring the Impact of the IRA

According to Energy Innovation, 400,000 clean energy jobs have been generated since the IRA was passed in 2022 and about $600 billion invested by the private sector into the industry. A two-year report card of the IRA published by Global Infrastructure Investor Association in September 2024 estimated that the IRA directly spurred $115 billion and created 90,000 jobs in the first two years of its signing, proving to be a key variable in the future of American energy.

At the beginning of the IRA’s effective period, American Clean Power Association estimates expected it to more than triple domestic clean energy production, adding 525 GW – 550 GW of new clean energy generation by 2030. This meant that bolstered by IRA incentives, the clean energy industry would grow over the next four and a half years to provide over 40% of all electricity in the country.

An Analytical Look at the OBBBA

The signing of the OBBBA into law has heavily disrupted planned investment and development and changed the projections regarding greenhouse gas emissions reduction, clean energy, infrastructure, investment outlooks, and other factors that had gone into long-term planning and forecasting. A full economic analysis of the OBBBA awaits us in the future, but it is safe to say that the new Act will slow solar and wind development and have major implications for the broader industry, posing challenges and cost increases for many States and businesses that have set aggressive renewable adoption goals.

A first quantitative look at potential outcomes of the OBBBA, assuming it runs its course through 2034, reveals a mixed bag. The elimination and restriction of tax credits are estimated to raise just under $500 billion in revenue during 2025-2034. Accounting for the rollback of, or increased restrictions, on EV credits, residential and commercial building efficiency credits, and clean hydrogen production credits, the total revenue generation during the period specified above could turn out to be $543 billion.

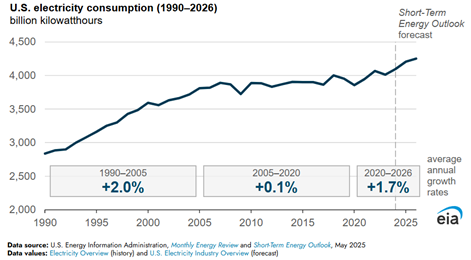

The rise of data centers and the electrification of buildings and transportation are driving up electricity demand across the country. According to the National Electrical Manufacturers Association, U.S. electricity demand will grow by 50% by 2050, with data centers quadrupling their energy consumption over just the next ten years. The EIA graphic below shows the historical growth in domestic electricity consumption as well as the near-term projections for the same. In light of these forecasts and existing market economics, many renewable energy advocates are critiquing the OBBBA for raising the cost of new electricity generation.

Figure1: U.S. Electricity Consumption during 1990-2026 (Source: Energy Information Administration)

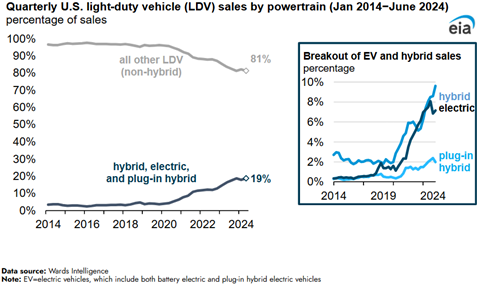

Another trend that stands to be impacted by the OBBBA is EV adoption in the United States. With EV credits being terminated eight years earlier than expected, Americans are more likely to buy gas-fueled cars, which is expected to drive up demand and potentially the price of gasoline. The following chart from the EIA shows the recent surge in EV and hybrid vehicles sales in the U.S. while traditional vehicle sales slumped simultaneously. In the coming years, this chart could display dramatic movement.

Figure 2: Light vehicle sales trend in the U.S. during Jan 2014-June 2024 (Source: Energy Information Administration)

It is physically impossible to keep a detailed breakdown of the impacts of the OBBBA within the length recommendation for a palatable blog post, so I will jump to the expected environmental outcomes in an energy landscape guided by the OBBBA. It is important at this stage to separate myth from fact and not judge a book by its cover. While widely touted as a poison pill for the green movement in the country, the OBBBA does have a few elements that suggest otherwise.

The OBBBA enhances carbon capture and sequestration credits to ensure parity in tax credits for all uses of sequestered carbon dioxide, removes prevailing wage and apprenticeship (PWA) requirements for fuel cells to qualify for tax credits, slightly expands fuel cell credits, and leaves the IRA tax credits largely intact for energy storage technologies and nuclear energy. Almost all technologies, with notable exceptions including clean hydrogen and thermal storage, however, have been slapped with an expanded Foreign Entities of Concern (FEOC) restriction, which cuts out from tax benefits any projects with connections to or receiving material assistance from certain foreign entities as identified by the Treasury Department. The specific implications and potential ramifications of this more aggressive FEOC restriction will depend on how it is implemented by the Treasury Department.

Combined with the few enhancements of IRA provisions, the sharp cuts in tax breaks for EVs and clean energy are expected to have a net negative impact on greenhouse gas emissions over the next ten years. ClimateWork Maine reports this estimated impact in tangible terms, expecting these tax policy changes to increase GHG emissions by 310 million metric tons of CO2e by 2035. The replacement of EV demand and solar and wind energy capacity additions by the burning of fossil fuels will be a major culprit for the emissions impact. It remains to be seen how state-level policy or other market forces respond to this massive change in federal incentives.

Conclusion

To conclude this summary of the changes implemented by the OBBBA, we can focus on two aspects – timelines and foreign-influence. Most projects that have already begun construction should be able to safe harbor the original IRA tax credit values – stackable bonuses for projects located in energy communities and satisfying prevailing wage and apprenticeship requirements remain intact, and credit values remain unchanged.

However, those projects that are in earlier stages of consideration or prospective projects for future years will have to contemplate how they will adapt to the OBBBA changes and await further guidance on FEOC restrictions.

The Treasury Department has been directed by a Presidential Executive Order as of July 7, 2025, to provide more guidance on executing the OBBBA and is expected to provide more clarity and direction as to how the legislation will be interpreted. Considering recent global geopolitical volatility, evaluating the impact of the Act on capital planning, PPA pricing, state RPS requirements, foreign investments into the country, energy jobs, and other macro and microeconomic factors will be a dynamic and challenging task in the months ahead.

If you have questions about how these energy policy changes may affect your business, please contact one of our Energy Services Advisors today.

Photo by Ridvan Celik