By Max Webb, Managing Director of Pricing and Zack Hallock, Senior Energy Services Advisor

We’re back with another installment of our winter weather forecast. Before diving into this year’s forecast, we first need to take a step back and recap last winter—when the U.S., and specifically New England, was in a very different position compared to where we are today.

As you may remember, the Ukraine/Russia conflict dominated the news in the summer and fall of 2022, which turned energy markets upside down and reordered the global energy status quo. In tandem with the trouble overseas, the U.S. was well below the five-year average for natural gas storage, which normally is a precursor to energy price spikes heading into a New England winter. The global climate weather phenomenon, El Niño-Southern Oscillation (ENSO), was in a rare third consecutive year in the La Niña phase, which resulted in many weather forecasters raising alarms for a cold 2022-23 winter ahead. As a result, New England saw unprecedented energy price spikes and volatility throughout the summer heading into the winter.

So, what happened? Well, the winter of 2022-23 was one of the warmest winters on record for New England. After getting through January without any extreme or prolonged cold, the energy market reset, resulting in drastic energy price drops in early 2023.

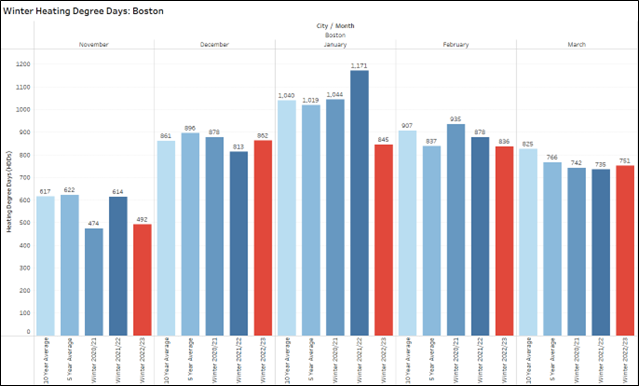

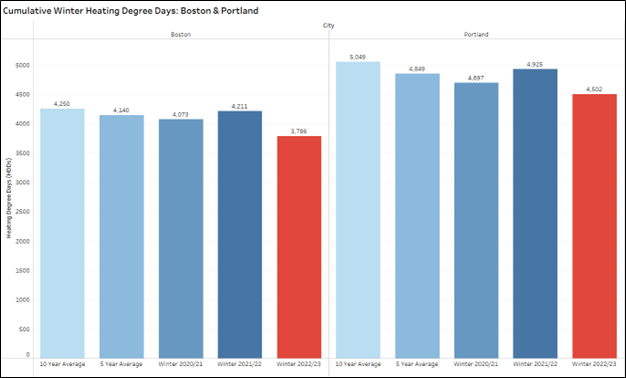

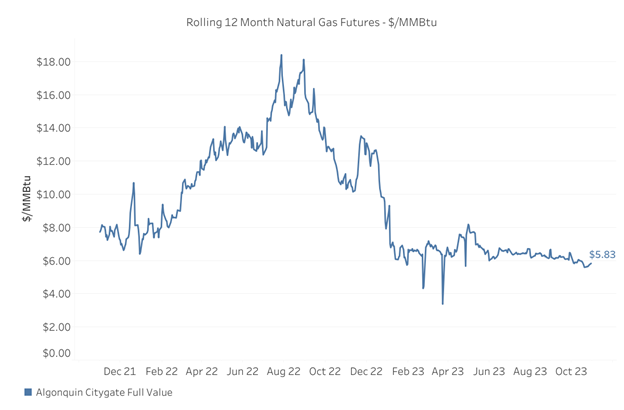

Figures 1 & 2 compare Boston and Portland winter heating degree days over the last few years as well as the most recent 5- and 10-year averages. Shown in the red bars, last winter had far fewer heating degree days than the previous two winters. For comparison’s sake, Figures 1 and 2 also depict 5- and 10-year winter heating degree day averages. Figure 3 shows the natural gas price trend where they fell off a cliff at the end of December and into the New Year largely due to warm temperatures.

Figure 1: Winter (Nov-Mar) Heating Degree Day History for Boston

Figure 2: Cumulative Winter Heating Degree Day History for Boston & Portland

Figure 3: Natural Gas 12 Month Rolling Strip

As shown in the graph above, energy prices have been relatively stable since the drop in early 2023. However, it seems the market is almost waiting for the next major event to cause another drop or spike.

Which will it be, a drop or a spike? Looking at the upcoming winter weather forecast may give us an early indication. We’re focusing on a few key factors such as the La Niña to El Niño transition, the polar vortex, and other influences such as sudden stratospheric warming events and the Quasi-Biennial Oscillation. We use these indicators to get a read on bearish or bullish factors, and their potential market impact.

ENSO: La Niña to El Niño

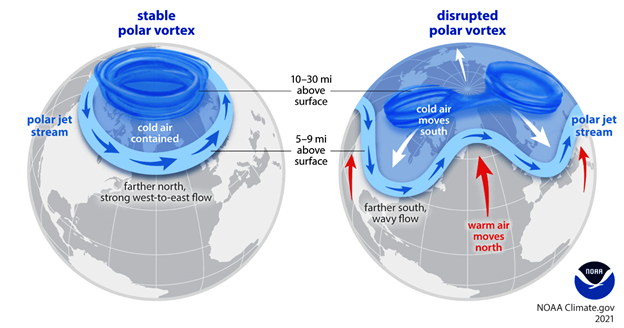

The largest scale feature of winter weather in North America and Europe is the spectrum of warmer or cooler Pacific Ocean surface temperatures along the equator. This drives the El Niño Southern Oscillation. Along this spectrum, there are two commonly known phases, La Niña & EL Niño with the occasional neutral winter in the mix as we oscillate on the spectrum every three-to-five years. Interestingly, we just experienced three consecutive La Niña winters and are now experiencing a quick transition to El Niño. This is significant because El Niño winters often reflect the weakening of easterly (from east to west) winds and can even develop westerly (from west to east) winds in the Pacific Ocean that bring a large amount of warm and moist air to the continent from the Pacific. Typically, we see easterly winds along the equator in North America, which has been true for the last three years. The changes in the trade winds are supported by an upper atmosphere low pressure feature in the North Pacific which keeps the pacific jet stream from being interrupted by the polar jet stream. The dance between the Pacific jet stream and the polar jet stream over North America is a major difference between the two phases of ENSO as shown in Figure 4 below. The last three years of La Niña have been characterized by a high-pressure blocking feature over the North Pacific which pushed the polar jet stream deep into the continent and gave resulted in some legitimate cold anomalies across the continent.

Figure 4: El Niño Vs. La Niña Jets Stream Features and Impact on Temperature/ Precipitation

ENSO Price Impact: Bearish

Often, moderate to strong El Niños lean toward warmer than average winter temperatures for North America. An El Niño doesn’t protect us from all cold spells, and in fact, the eastern half of the United States is forecasted for below average temperatures over the first half of November. Thankfully, the early November cold has not caused much movement in energy prices to date. The overall warm winter forecasts, largely influenced by El Niño, have helped keep a lid on prices throughout the fall and heading into the winter.

Sudden Stratospheric Warming & Quasi-Biennial Oscillation (QBO)

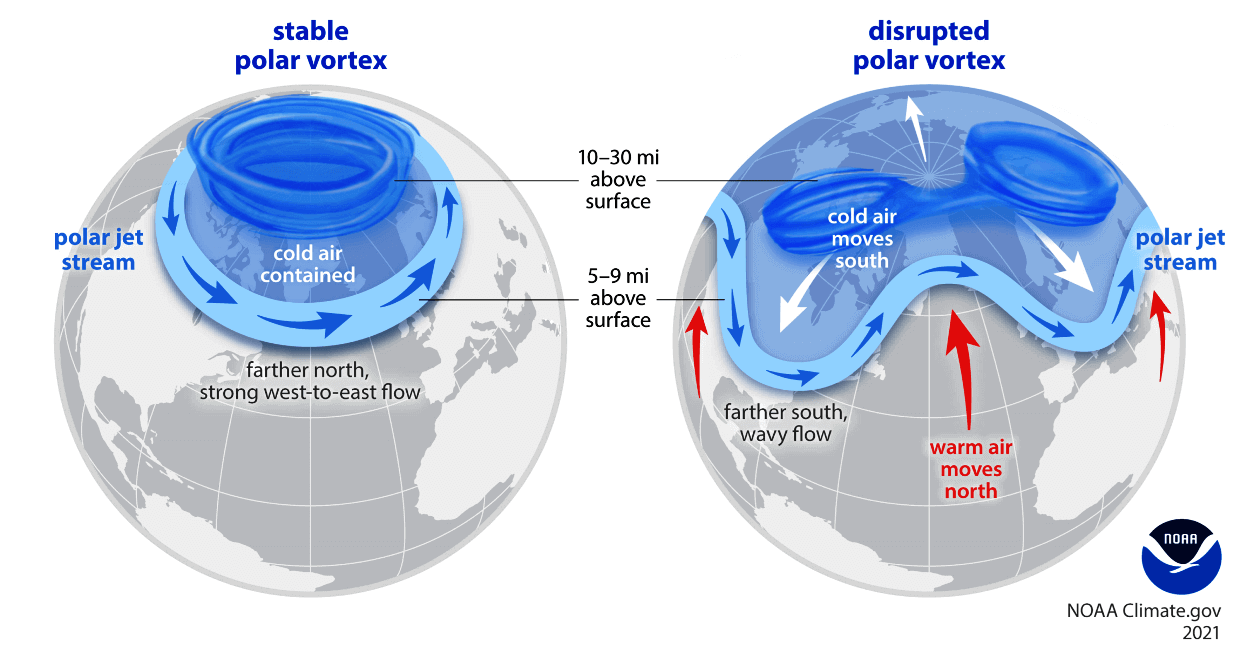

Don’t bank on lackluster heating demand all season. The back half of winter is too far out to put a high degree of confidence on the warm anomaly expectation, mainly due to the variability of Sudden Stratospheric Warming (SSW) events and the recent change in the Quasi-Biennial Oscillation (QBO). SSW events are not a common occurrence but have immense potential for disruption to temperatures in North America by fragmenting the stable polar vortex and pushing the polar jet stream south. Both La Niña & El Niño features are prone to SSW events, so this is not just an El Niño phase anomaly. However, polar jet stream disruptions can be amplified during the El Niño phase by the QBO.

Figure 5: Breakdown of Polar Vortex Due to Upper Atmosphere Sudden Stratospheric Warming Event (SSW)

{kind=link}

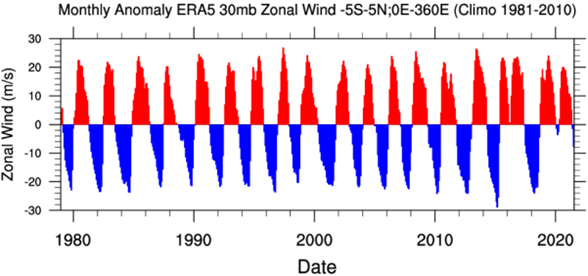

The QBO is a Stratospheric wind pattern that oscillates every 12- 14 months. The QBO shifts from a westerly or “positive” direction to an easterly or “negative” direction surprisingly on a wildly consistent basis back to 1980. The consistent pattern is shown below in Figure 6. Note the start of a negative cycle in blue at the far right of the graph, showing a recent shift to easterly winds at around 25km/15 miles above the equator.

Figure 6: Stratosphere Zonal Wind Anomalies Above the Equator (1980- 2023)

An easterly QBO increases the likelihood of SSW events because it is simply working against the westerly flow of both the polar jet stream and the polar vortex, which always move westerly regardless of the ENSO phase. These competing upper atmospheric forces lead to a higher likelihood that the polar vortex will be fragmented and deliver significant cold intrusions to the northern hemisphere.

SSW & QBO Price Impact: Bullish

If any SSW events materialize this winter, it would certainly increase prices, however, the increase would mostly be felt in the near-term spot market. There would also likely be a short-lived ripple effect in the futures market, but those price spikes should subside once milder temperatures return in the spring. These SSW events and corresponding cold intrusions will be a key factor to monitor, especially for clients who have any open energy positions, exposure to the spot market, as well as those with dual fuel capabilities for arbitrage and fuel switching. In previous winters that were El Niño with a negative QBO, the northeast saw multiple cold intrusions pushing against the warmer trends the rest of the country felt. A good example is winter 2009-10.

NOAA Temperature Outlook

With all the above in mind, what are weather experts predicting for winter 2023-24? The clear answer is we should expect an above average temperature pattern this winter across the whole of North America, with one caveat. Significant cold intrusions are expected in the northern United States, particularly the Northeast. National Oceanic and Atmospheric Administration (NOAA) shares a similar view in their Three-Month Outlooks.

Below we have both the three-month (December - February) and the three-month (March- May) temperature anomaly predictions. Clearly NOAA agrees that the El Niño feature will dominate with a warm trend that weakens as we progress into the spring. Again, these are three-month averages so a one-to-two-week cold intrusion should still be expected from time-to-time.

Figure 7: NOAA Seasonal Temperature Outlook, Dec-Jan-Feb 2023-24

Figure 8: NOAA Seasonal Temperature Outlook, Mar-Apr-May 2024

NOAA Temperature Outlook Price Impact: Bearish

The overwhelming theme in these long-range forecasts is above average temperatures for much of the country, including New England. Even though the northern U.S. is likely to receive some stretches of cold air due to a weakened polar vortex, the strength or frequency of those cold periods is not forecasted to outweigh the warmth. As a result, the overall price signal is bearish, especially if it takes until January or February before any significant or extended cold appears. In that case, robust natural gas storage and more readily available, cheap LNG should be more than enough to heat us through the winter resulting in less pressure on the energy grid and market.

Key Takeaway and Next Steps

The current warmer weather forecasts correlate with downward pressure on national energy prices, particularly in New England. That said, with winter comes cold weather. Undoubtedly, there will be cold stretches that impact much of the U.S. and it would be unwise to write off old man winter based on the above projections. Still, if these warm forecasts turn out to be true, then some degree of price relief in early 2024 can be expected.

There’s no question that weather fluctuations impact energy pricing and it’s something that CES monitors with regularity. Weather, however, is just one factor to consider when making energy-related decisions. Other important factors add to the complexity and volatility of energy pricing. For example, geopolitical tensions will almost certainly cause volatility in the market. That’s where CES can help you most. As we move into the winter season ahead, please feel free to contact a CES Energy Services Advisor to discuss your unique energy needs and to devise a game plan to get you through the winter and beyond.