By Max Webb, Managing Director of Pricing Analytics

Back in February 2023, Larry Pignataro and I co-authored a blog titled, Fuel Security: New England’s Biggest Winter Concern, inspired by a topic that CES clients regularly ask about and one that is a constant in today’s changing energy landscape.

Though winter is well behind us, the topic of fuel security is an ever-present conversation at Competitive Energy Services. With summer approaching, I wanted to provide an update on New England’s fuel security programs. Fuel security and grid reliability concerns are not unique to New England, so I will also highlight how some Independent System Operators (ISOs) across the country are tackling this issue along their way to decarbonizing their electric grids.

What is Fuel Security? A Recap

Fuel Security is a concern across the country as we decarbonize energy systems, switching from legacy fossil fuel sources of power generation to low and zero carbon alternatives. As coal, oil, and dual fuel power generation assets retire – making way for solar, wind, and battery storage – regional grid operators need to make sure that enough fuel will be available to power plants at the right time and location.

The Independent System Operator of New England (ISO New England) has instituted a “fuel security” program that permits them to retain certain generation assets during peak winter events to ensure system reliability and the fuel used to run those assets. The two current Fuel Security programs in the New England region are: Mystic Cost of Service and Inventoried Energy.

Almost a year-and-a-half after our last blog on fuel security, where these programs were relatively new, there are still questions and overall uncertainty about the future of each program. Below is an update on ISO-NE’s two fuel security programs, along with similar initiatives in other regions of the U.S.

Mystic Cost of Service Update

The first of the two fuel security programs is known as Mystic Cost of Service. This program was created to delay the retirement of the Mystic Generating Station, a large generator located outside of Boston, for an additional two-year period from June 2022 through May 2024 due to grid reliability concerns created by the retirement. The Mystic facility provided fuel security thanks to its location near the Boston load center and because it did not rely on pipeline natural gas – instead it was fueled by liquified natural gas (LNG) imported on large tanker ships and stored in onsite tanks. Because New England has insufficient pipeline capacity to meet both heating and power generation needs on peak winter days, the Mystic Plant provided a source of generation that used an alternative fuel that could be stored onsite. To keep Mystic operational, the Mystic Cost of Service program was funded by charges that all New England electricity end users have been paying through the supply side of electricity bills.

Now that we are a few days beyond the end date of the program, let’s look back at just how much this could cost. Note, not all Mystic Cost of Service charges are known due to a two-to-three-month lag between when the costs are incurred and when they are officially announced publicly. There is also a reconciliation period which allows the ISO to tweak these costs over a period of a few months.

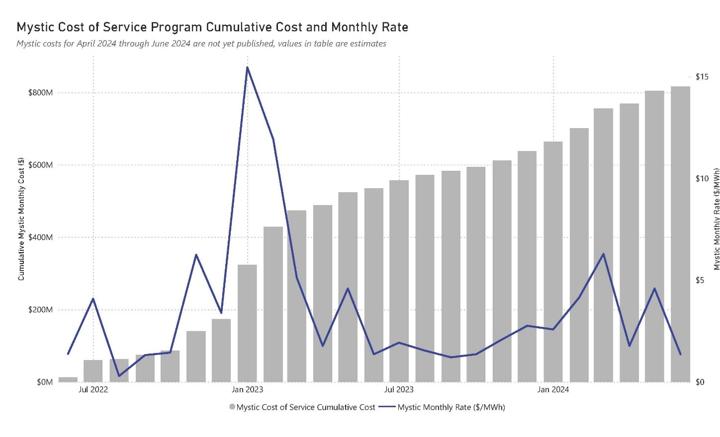

Figure 1: Mystic Cost of Service Program Cumulative Cost and Monthly Rate ($/MWh)

Shown in Figure 1, the Mystic Cost of Service program cost more than $755 million dollars from June 2022 through March 2024. This correlates to $3.48/MWh paid by all New England electricity end users. The final cost of Mystic will likely exceed $800 million, including estimated costs for the last three months of the program. While this is a large sum of money, it could have been far more expensive, which was the original fear in the energy industry just a couple of years ago when the program was being implemented.

The large rate spike seen in Figure 1 was strongly correlated to high costs of LNG, Mystic’s primary fuel source. January and February 2023 costs make up more than $250 million of the $800 million total cost of the Mystic Cost of Service program. Thankfully, the high LNG prices were relatively short lived and have since dropped closer to historical average prices.

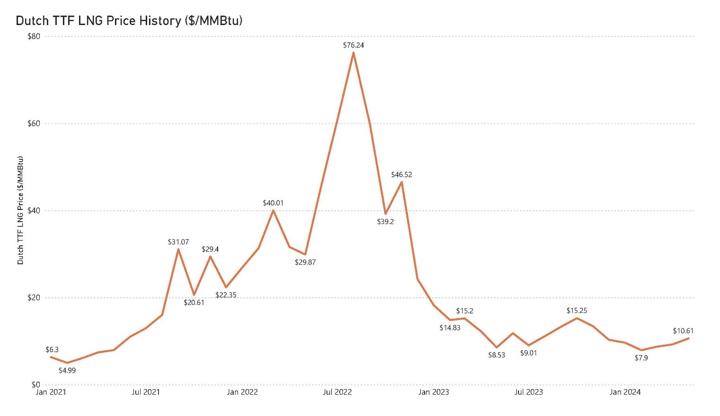

Figure 2: Dutch TTF Liquified Natural Gas Price History (January 2021 to May 2024)

Shown in Figure 2, and starting with the Russian invasion of Ukraine, global LNG prices started to climb in early 2022 and peaked during the summer and fall of 2022. Sanctions imposed on Russia, including natural gas exports, brought concerns of global natural gas supply shortages which drove prices up heading into the upcoming winter. Thanks in large part to mild winter weather that year, natural gas inventories ended the season higher than forecasted and helped relieve pressure on pricing. Since winter 2022-23, LNG prices have returned to closer to historical average.

As a result of the lower LNG prices, Mystic monthly rates have generally bounced between $1-4/MWh and consistently stayed below $50 million per month.

Even though New England experienced overall warm winters in 2022-23 and 2023-24, there were still some extreme cold weather events where Mystic was dispatched to generate electricity to help keep the lights on. If Mystic were to have retired originally as planned, New England may have faced higher energy prices during those cold weather events, forced energy consumption curtailment, and even rolling blackouts.

Inventoried Energy Program Update

Moving on to the second of the fuel security initiatives, Inventoried Energy Program (IEP). The purpose of IEP is to help ensure that participating generators have enough fuel stored on site during peak winter periods to meet demand. Qualified generators are reimbursed to cover their cost of storing extra fuel for the winter periods if they can prove they are eligible. The program targets two winters: December 2023 – February 2024 and December 2024 – February 2025. Like the Mystic Cost of Service program, IEP has an unknown element to its final cost due to the variable nature of fuel costs, however, IEPs cost parameters are better defined than the Mystic program. Plus, there is a cap on the total possible cost.

During the first winter of IEP (winter of 2023-24), costs came in just above $75 million and monthly rates ranged from $2.45-2.66/MWh, which was far less expensive and volatile than the Mystic Cost of Service. Looking forward to 2024-25 winter, IEP rates will again depend on what happens with winter weather and fuel costs. However, now that we have collectively experienced one winter of the program, most suppliers are comfortable with how this program works and how much it will likely cost, so there is less concern in the supply marketplace. The current thinking is that 2024-25 IEP rates should be similar or slightly lower than 2023-24 due to the relatively stable and less expensive LNG fuel costs and robust natural gas storage inventories.

What’s Next for New England?

The Mystic Generating Station is now officially retired. As previously mentioned, Mystic’s primary fuel source was LNG, which they received by cargo shipments through the Everett LNG import terminal located just down the road. Mystic was Everett’s main customer, so there was fear that with Mystic going away, Everett would follow suit and New England would lose its primary option for importing LNG. This again raised fuel security concerns with New England’s lack of natural gas availability during peak demand periods.

To solve that issue, at least for a little while longer, the Massachusetts Department of Public Utilities recently approved agreements between Everett and the regional natural gas utilities Eversource, National Grid, and Unitil to keep the LNG terminal around for another six years. It is not known at this time how much these agreements will cost, or how these costs will be collected from natural gas and/or electricity consumers, but it is a price that New England energy consumers will have to pay for a reliable, albeit likely expensive, natural gas fuel source.

As for the Inventoried Energy Program, we have one winter to go, and at this time there is no concrete plan for winters beyond 2024-25. The program was designed to be a short-term solution to this larger fuel security problem; however, it seems likely that IEP is either extended for at least an additional winter or replaced with a modified or new fuel security program.

To help ease any remaining concerns, here’s a recent quote from ISO-NE spokesperson Matt Kakley, “Our analysis has shown that in the short- to-medium-term the region is in good shape," Kakley said. "What you're seeing right now in New England is really a pivot point in terms of the transition to a clean energy grid that the region is seeking."

Beyond New England

As mentioned in the introduction – fuel security and grid reliability concerns are not unique to New England. For the purposes of this article, I am focusing on two of the larger independent system operators who are leading the way on the journey to grid decarbonization.

ERCOT

The Electric Reliability Council of Texas (ERCOT) has been building wind and solar farms at an enormous scale. ERCOT has more than 26,000 MW of solar, battery storage, and wind capacity scheduled to come online in 2024. For context, the peak load in New England during 2023 was about 24,000 MW. This is an impressive feat and important progress toward a cleaner electric grid; however, those additions bring fuel security concerns along with them. While there is no significant fossil fuel generation scheduled for retirement this year, the growth of and added reliance on renewable energy in ERCOT increases the likelihood of fuel security related events. Solar and wind generation is non-dispatchable, meaning that they only generate electricity when the sun is shining, or the wind is blowing. Fossil fuel generation can, in theory, generate on-call, but they typically require hours to days’ notice to get up and running and have also suffered from outages during cold weather events due to inadequate weatherization. This can make it difficult for grid operators to balance the grid as unplanned outages, shortened maintenance periods, frequent extreme weather events, and many other factors are causing a tighter supply and demand balance. Recent examples of such events can be seen with Winter Storm URI in 2021 and the 2023 record setting summer peak demand of 85,508 MW, both of which resulted in extreme price spikes and rolling blackouts. Similar to New England, ERCOT will look to delay retiring fossil fuel generators since they are so critical during these peak periods, at least until energy storage systems are available in sufficient quantity or other “clean firm” resources are available.

CAISO

The California ISO (CAISO) has also developed large amounts of renewable energy capacity over the last decade plus. Just this year, CAISO is expected to bring on almost 7,000 MW of battery storage capacity and almost 5,000 MW of solar capacity. Battery storage is a crucial element to CAISO due to the amount of solar capacity in their grid mix. During the day when the sun is seemingly always shining in California, the massive amount of solar generation serves the majority of day-time demand. The massive amount of solar generation has moved the daily and system grid peaks to later in the day. As a result, California is opting to store solar generated in batteries for use during the morning and evening peak load hours. They will then dispatch the battery in place of carbon-based generators during the morning and evening peak periods. This results in lower emissions and cheaper costs during the peak, which is a net positive compared to using fossil fuel based peaking generators. Even at the pace that CAISO is building wind, solar, and battery capacity, it is not enough to satisfy all near term grid reliability concerns. Just this year, a nuclear generator and multiple gas fired generators that were scheduled to retire have had their retirement dates extended out multiple years.

Conclusion

CAISO is ahead of the most other regions in terms of the decarbonization of their electric grid, but the issues they still face provide a reminder to the rest of the U.S. that a carbon-free grid is difficult to achieve. New England will continue to push toward a carbon-free grid while also pushing for the electrification of heating and transportation. The key takeaway and lessons learned from CAISO and ERCOT is that while time is coming to an end on Mystic Cost of Service and Inventoried Energy Program, there will be new, costly programs that arise to help bridge the gaps.

As always, CES is in tune with both energy markets and regulatory events that have an impact on our clients, so stay tuned for future updates on fuel security and grid reliability. If you have any questions or would like to learn more about fuel security or any regulatory events, please feel free to contact the CES Energy Services Advisory team.