By Aaron Rubin, Senior Energy Analyst

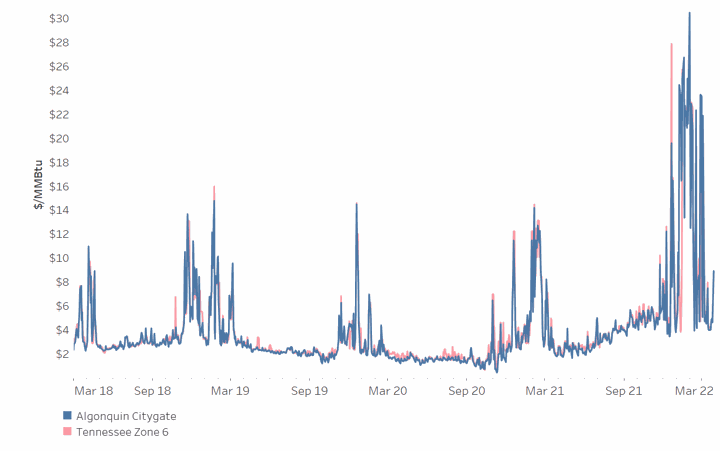

In January through February of 2022, New England’s spot natural gas prices at Algonquin City Gate climbed to $16.55/MMBtu, the highest combined average daily price settlement for these two months since winter 2014. With natural gas-fueled power plants establishing the clearing price for New England’s wholesale electricity market, the upward trend in natural gas prices also drove electricity prices to their highest point since 2014 at $149/MWh in January and $114/MWh in February. These consistently high daily energy prices diverged drastically from the historic lows set in recent winters, posing significant operational challenges for regional businesses already faced with surging raw material costs as supply chain problems persist.

With the war in Ukraine leading Europe into a potentially worsening global energy crisis, there is a growing need for businesses to understand the market fundamentals that caused New England spot energy prices to reach decade highs this winter. Developing an understanding of these concepts is critical for companies interested in designing energy cost containment strategies for future winter heating seasons since shifts in market fundamentals that impacted prices this winter are now driving up energy prices for future winter seasons. Currently, the full-value futures pricing for Algonquin Citygate sits at $21.23/MMBtu for winter 2022-23, up more than 75% since the start of November 2021.

Figure 1: Trends in historical spot natural gas price settlements in New England at Algonquin Citygate & Tennessee Zone 6. Daily price settlements at Algonquin Citygate averaged $20/Dth in January and $13/Dth in February. The previous Three-year historical price settlement averaged ~$5/Dth daily for these two months.

As outlined in my colleague Simon Pritchard’s article, New England gas markets are susceptible to high prices during peak heating season when the region’s limited pipeline infrastructure is not adequate for meeting demand on colder winter stretches. This January brought some of the coldest weather New England has experienced in recent years, with Boston recording the lowest average monthly temperature since January 2009 (27.4F). These frigid temperatures spurred a month of significantly above-average heating demand that persisted into mid-February. During long periods of cold temperatures with high heating fuel demand as occurred this winter, New England’s energy markets must supplement pipeline gas with liquefied natural gas (LNG) and oil to meet total demand. This backstop has made New England energy markets susceptible to any volatility seen in global LNG prices, as New England must compete with international markets to attract LNG cargoes.

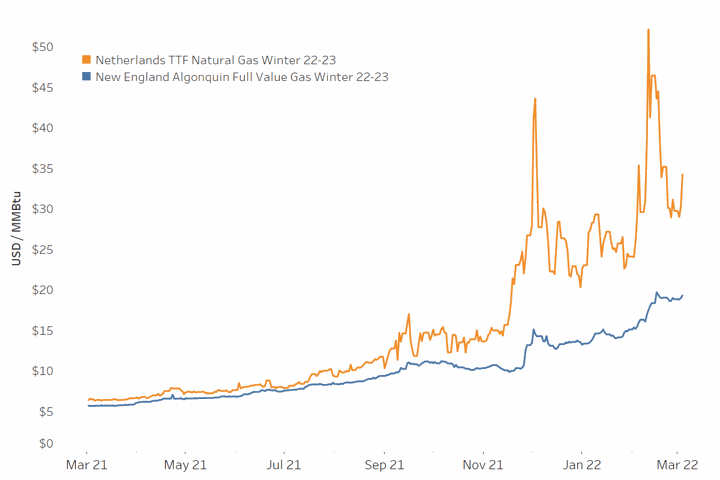

This history of susceptibility to LNG prices proved again to be the case this winter. This January, below-average natural gas storage inventories in Europe and supply risks caused by a deliberate reduction in Russian gas flows as tensions with Ukraine and Western Europe emerged, led European gas prices to skyrocket. The EU Dutch TTF European price marker consistently settled between $75/MWh and $90/MWh in January – February 2022, up more than 300% from the previous year that saw prices remain consistently under $25/MWh. As prices in Europe increased with the winter heating fuel shortage, New England’s ability to attract sufficient LNG cargoes came at a significant cost premium over previous winters as LNG cargoes could divert to sell the commodity in the more lucrative European markets. The shared reliance between New England and Europe on LNG deliveries has prompted concerns that a prolonged invasion of Ukraine could drive New England prices upward. The cause for apprehension here is evident when observing the interconnected movements between the Dutch TTF Winter 2022-23 strip and AGT Winter 2022-23 strip below.

Figure 2: Trends in European Natural Gas Winter 2022-23 Pricing vs. New England Full-Value Winter 2022-23 Pricing. Gas contracts are currently cheaper in New England than in Europe next winter. However, a clear trend exists in market movements between the two price points.

Cold temperatures this winter were likewise experienced broadly across the East Coast and the Midwest, signaling above-average heating demand for the entire nation. In addition to weather-driven demand, slowly recovering dry gas production numbers and high gas exports helped drive national storage levels well below the five-year seasonal average by the end of winter 2022. While these market fundamentals placed moderate upward pressures on futures pricing at the national price marker at Henry Hub in Louisiana (NYMEX), the increases on NYMEX this winter were very marginal relative to upward trends in New England basis futures pricing. This difference again speaks to the unique pricing conditions in New England that result from the region’s pipeline constraints and reliance on LNG deliveries.

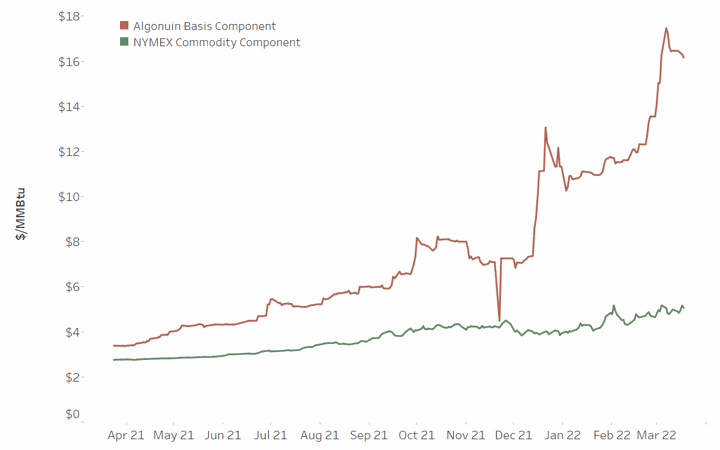

Figure 3: Winter 2022-23 Strip Pricing for New England Gas. Full gas value broken down into distinct NYMEX & Algonquin Basis cost components. It is the Algonquin Basis component of gas pricing (the differential between the price of gas in New England and the price of the national NYMEX marker) that drove New England’s gas prices up for future winters. NYMEX futures were less severely impacted by this winter’s energy market fundamentals, underscoring the impact of New England-specific pipeline constraints on the region’s gas prices.

The specific circumstances causing spot energy prices to escalate in New England this winter may continue in future years, as evident in the recent upward movement in winter futures strips for New England electricity and natural gas. In the near term, how the war in Ukraine unfolds will have the most significant impact on energy pricing in New England. The speculation that European countries could receive fewer energy imports from Russia and need to supplement with other resources, such as heating oil and LNG, has already pushed New England's future winter energy pricing upward. International demand for LNG is likely to remain high even if Russian gas flows to Europe hold steady as part of Europe’s strategy to reduce its dependence on Russian gas. This is evident in Germany’s recently announced plans to build out two new LNG import terminals aimed at reducing the country’s dependence on Russian gas imports. This rising global demand for LNG is apparent even for outer pricing years for Massachusetts, as winter 2025 and winter 2026 strips are now trading at more than $12/MMBtu. So long as a higher demand baseline for LNG holds, New England is likely to continue to pay a winter premium for gas and electricity relative to the low prices seen over the last decade.

It also seems unlikely that New England will build out any additional pipeline capacity to help address high gas prices. The investment would be expensive and juxtaposed with state and regional goals and policies aimed at reducing fossil fuel reliance, as evidenced in aggressive regional RPS policies and electrification benchmarks. Achieving beneficial electrification could reduce New England’s dependence on international energy market fluctuations as natural gas gets phased out of the electricity and space heating fuel mix. However, the pathway to this point of energy independence may prove extremely costly in the coming decade if global energy prices remain high and New England's access to the Marcellus Shale remains limited by pipeline infrastructure. The speed at which the renewables transition occurs and causes gas demand to fall could thus be critical for the region’s energy future. Amongst other shifts in energy market fundamentals, the U.S. is likely to increase LNG capacity as investors in liquefaction facilities are rewarded with higher prices. Yet, there is no guarantee that more of this gas ends up in New England instead of in international markets.

For these reasons, pricing for future winters remains concerning for both businesses and residential customers in the New England region. The market volatility and future winter price risk reaffirm CES’ adamancy in the value of designing creative energy procurement strategies for hedging against market fluctuation. Long-term electricity and natural gas supply contracts may help protect businesses in circumstances where energy markets suddenly and unexpectedly shift upward. Other entities electing to purchase energy on the spot market can still limit price exposure by hedging portions of their projected energy consumption in the higher-priced winter months. CES also assists clients with fuel arbitrage and multi-fuel strategies that enable clients to switch between heating options (or even curtail anticipated energy loads) based on anticipated daily energy prices. Preparing to implement any of these types of energy management strategies in a volatile energy market can prove rewarding for institutions and businesses.

The price of natural gas and electricity remains uncertain in New England, as markets will respond in the coming decades to global price signals and the speed at which beneficial electrification occurs in the New England region. Our CES Energy Services team is always interested in helping organizations learn more about trends in futures energy pricing and brainstorm approaches to procurement that could help reduce exposure to energy market volatility.

Photo by Leonid Ikan