By Zac Bloom, Vice President, Head of Sustainability and Renewables and Sandy Beauregard, Director of Sustainability Services

The United States withdrew from the Paris Agreement for the first time in 2017, during President Donald Trump’s first term. This action spurred a strong response from corporations, universities, states, and municipalities to maintain the commitment to reducing global greenhouse gas emissions. Nearly 4,000 entities signed on to the We Are Still In pledge and many states enacted increased renewable portfolio standards (RPS) and clean energy standards. These actions highlighted the continued push toward a cleaner energy future despite the federal government’s stance.

In the first few months of his second term, President Trump has issued numerous policies and executive orders aimed at the energy sector, favoring fossil fuels while rolling back former President Joe Biden's climate policies and again withdrawing from the Paris Agreement. The pace of these executive actions has created a lot of confusion, and many are being challenged in the courts. While the legal process plays out, we have not seen the same type of public response reaffirming commitment to the goals of the Paris Agreement as we saw during Trump’s first term. As the dust begins to settle on some of these initial Trump administration policies and executive orders, some key questions remain: has the renewable energy landscape become any clearer? Are energy users’ actions regarding carbon mitigation and renewable electricity goals slowing down in response to the uncertainty and shifting federal priorities?

This blog explores how the U.S. renewable energy sector is evolving amid shifting federal policies. We’ll examine the economic factors driving the industry, the rise of renewable procurement methods, and how different market players are responding to both opportunities and challenges.

ECONOMIC CONSIDERATIONS

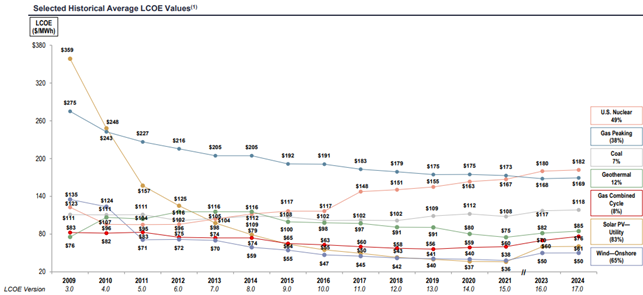

A key insight comes from Lazard’s annual Levelized Cost of Energy (LCOE) study. For the first time in more than a decade, the levelized cost of electricity for renewables saw back-to-back year-over-year increases and in 2024 the low end of the LCOE range increased for the first time ever. However, the long-term trend of decreasing renewable energy costs continued in 2024. It is important to note that the cost increases were not isolated to renewables; traditional generation sources such as gas peaking plants and coal faced rising costs as well. Despite the increase in LCOE over the past two years, the LCOE for utility-scale renewables has declined significantly over the past 15 years and they can be cost-competitive with conventional generation.

Figure 1: Lazard’s Historical Levelized Cost of Energy Comparison

Impact of High Interest Rates on Renewable Investments

These cost figures show that high interest rates and the inflated cost of capital have continued to impact investment and construction of new projects. Incentives available through the Inflation Reduction Act (IRA) have mitigated some of that impact, but uncertainty about the future of these incentives and other clean energy funding mechanisms under the Trump administration are likely to have as chilling an effect as we are seeing in other market sectors. Tariffs will drive up material costs and may disrupt supply chains, which were just beginning to correct following the disruptions from COVID-19.

Regardless of federal policy, electrical demand is expected to increase rapidly with the growth of data centers and development of artificial intelligence. Demand will also increase if Trump’s economic policies successfully promote onshoring and reindustrialization. This increase in electricity demand and consumption will need to be met with a diverse generation mix inclusive of renewables, energy storage, and dispatchable resources.

RENEWABLE GENERATION GROWTH

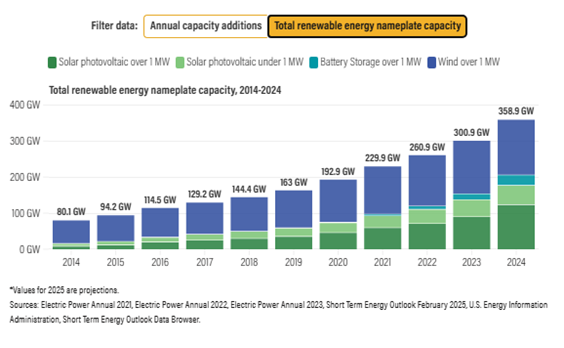

Looking back at 2024 in the United States, new renewable generation capacity totaled 57.8 gigawatts (GW), and the total renewable generation capacity reached 358.9 GW. Additional renewable capacity is expected to come online in 2025, despite the shifting economic and political environment.

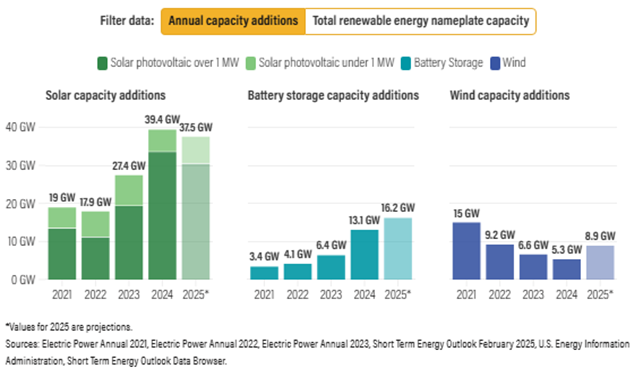

Figure 2: U.S. Renewable Energy Annual Capacity Additions and Total Generating Capacity by Source

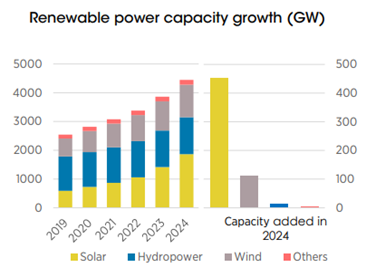

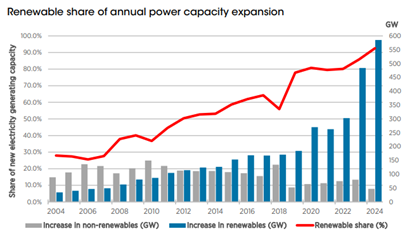

According to the International Renewable Energy Agency (IRENA), 585 GW of renewable capacity were added worldwide, accounting for over 90% of total global power expansion in 2024. These global figures show that renewables can compete with traditional generation sources and have been readily deployable.

Figure 3: Global Renewable Energy Annual Capacity Additions and Renewable Share of Annual Power Capacity Additions[1]

RENEWABLE PROCUREMENT

More barriers to renewable energy have been removed, creating broader access to renewable energy instruments. Previously, energy users seeking renewable energy options often turned to Green-e certified Renewable Energy Certificates (RECs) from existing renewable generators. These RECs could be from existing large-scale solar and/or wind projects anywhere in the U.S. This option offers low costs but sacrifices additionality and may sacrifice geographic proximity. Large energy users could also engage in a long-term virtual power purchase agreement (VPPA) with a project developer to construct a new renewable generator. These offsite projects could range in size from small community-scale solar (5 - 10 acres) to utility-scale generation projects (250 - 500+ acres).

The Rise of VPPAs and Tariffs

Given the contract duration and complexity, VPPAs have traditionally made sense only for large users with strong internal teams. While VPPA contracts continue to be popular with major companies like Google, Meta, and Amazon, smaller corporations are also starting to explore these options. Smaller users may be able to aggregate load and negotiate common contract terms with a large project or contract for a small share of a project anchored by a large off taker.

At the same time, the use of unbundled Green-e RECs has declined, giving way to more green tariffs offered by utility companies and community choice aggregators. Enrolling in a green tariff program is a streamlined process and does not require an energy user to contract with a different entity to supply renewable electricity. They also typically have short contract terms and can be easily terminated if priorities shift, different options become available, or the costs become prohibitive. This flexibility is appealing to many companies that are unlikely to execute a long-term contract.

Retail Suppliers Evolving

Retail energy suppliers are working closely with developers to create custom products for traditional electricity supply agreements. These agreements may involve renewable generation assets already in the supplier's portfolio or new projects that are under development. Depending on the generation source, these products allow users to trace their renewable purchase to a specific source and possibly make additionality claims. They also reduce the internal burden for a company to be able to review and commit to long-term contracts with the project developers.

Additionally, language can be included in retail electricity agreements to ensure that statutory requirements for renewable portfolio standards (RPS) are met through the purchase of RECs, instead of relying on alternative compliance payments. This allows users to take credit for the RECs being retired on their behalf by suppliers to comply with RPS requirements. Users are paying for these compliance RECs through the supply agreement and should be able to claim them in their own renewable energy and carbon accounting. We are seeing a growing need for this language as users seek to meet climate goals while managing costs.

CONCLUSION

So, is it different this time? While the call to action may not be as loud as it was during Trump’s first administration, the momentum in the renewable energy sector remains undeniable. The economics are clear: the levelized cost of energy for renewables allows them to compete with traditional energy sources — not just because of policy or public interest, but because it simply makes financial sense.

On both a national and global scale, renewable energy dominates new capacity and connection queues, further solidifying its role in the future of energy. Additionally, with more tools and instruments available than ever before — such as green tariffs, VPPAs, and RECs — the pathways to a renewable-powered future are more accessible.

That said, challenges remain. There are concerns about the future of clean energy tax credits, supply chain cost & availability impacts from tariffs, rising borrowing costs, and a capital market that had matured from its nascency, but now has foreign and domestic investors alike questioning the safety of their investments. While the flurry of activity in the renewables space signals progress, the future is anything but predictable. One thing is certain, however: the transition to renewables is ongoing, long term in nature, and its momentum is driven by more than just policy. It’s driven by economics and a changing energy landscape.

As we navigate this uncertain future, one thing remains clear: renewable electricity is here to stay, even if the path forward remains a little unclear.

Photo by: Pawan Thapa

[1] Renewable Capacity Statistics 2025, International Renewable Energy Agency. https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2025/Mar/IRENA_DAT_RE_Capacity_Highlights_2025.pdf