By Andy Price, President and COO

Russia’s invasion of Ukraine has been a humanitarian tragedy. The world has watched in horror at the millions of refugees, thousands of military and civilian deaths and the destruction of Ukraine’s infrastructure, but also in admiration at the unity and resolve of the Ukrainian resistance. As energy analysts, it is our job to study the war’s influence on energy markets and to consider both near- and long-term impacts for our clients.

Some effects of the war have been obvious and immediate. The price of gasoline and most liquid fuels spiked to near record highs as soon as the war began and have remained elevated ever since. As the third largest producer of oil in the world, behind only Saudi Arabia and the U.S., Russian exports are very important to world oil markets. Russia exports around 7.5 million barrels of crude oil and oil products each day to Europe, China, and other countries.

The U.S. banned all imports of Russian oil on March 8, but the ban is largely symbolic. Before the war, Russian oil accounted for only around 3% of U.S. supply and the oil can be replaced with relative ease. Due to the fungibility of oil and our existing refining infrastructure, however, geopolitical events in far flung areas of the globe can have immediate impact on gasoline and heating oil prices in the U.S. This is true even though U.S. energy production exceeds energy consumption on a net annual basis and even when the U.S. is not sourcing any oil from the regions in conflict. Oil is relatively easy to ship to the highest priced markets in the world and so gasoline, heating oil, and other liquid fuel prices in the U.S. have increased to near record highs because of the conflict in Ukraine, matching the increase experienced in other world markets. Crude oil has remained well over $100 per barrel since the war started and heating oil and gasoline are between $4 and $5 per gallon in most markets. California leads the U.S. with gasoline prices near $6 per gallon.

Other consequences of Russia’s invasion of Ukraine are less intuitive, such as the increase in U.S. natural gas and electricity prices, as well as disruptions to solar, wind, and other clean energy markets.

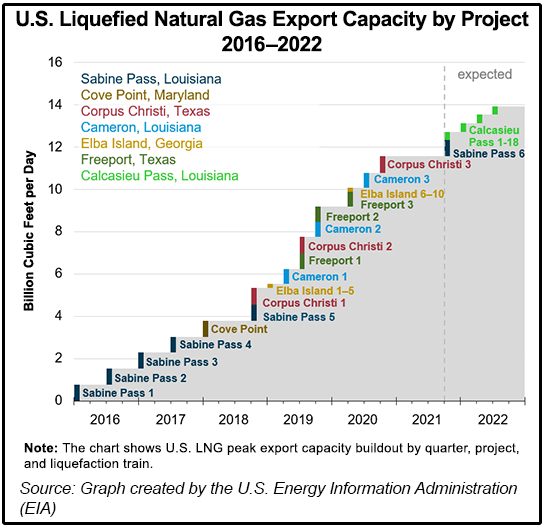

Natural gas has historically been a domestic market in the U.S. and, unlike oil, largely insulated from worldwide geopolitical issues. This started to change in 2016 as the first U.S. liquified natural gas (LNG) export terminal began operating in Louisiana. By chilling domestically produced natural gas to negative 260 Fahrenheit, export terminals turn natural gas into a liquid, increasing its energy density enough to ship the fuel around the world. Thanks to LNG, low-cost U.S. shale producers now have access to higher priced markets in Europe, Asia, and South America. As shown in the following chart, the U.S. now has seven major LNG export facilities – currently operating near full capacity - with the capacity to export up to 12 billion cubic feet (Bcf) of gas each day. To put this in context, every day the U.S. is exporting more than two times the amount of natural gas consumed in all New England on the coldest winter day. This export capacity will continue to grow as additional export facilities along the U.S. Gulf Coast currently under construction are commissioned.

The U.S. is expected to be the largest exporter of natural gas in the world in 2022. With total U.S. natural gas production expected to average 95 Bcf per day in 2022 – about 14% of domestic natural gas production is now sailing to foreign markets on large tanker ships. Thanks to the rapid proliferation of LNG export terminals in the U.S., Australia, and Qatar - as well as import “regassification” terminals in Europe, Japan, China, South Korea, and India - natural gas has quickly joined oil as a commodity whose price is heavily influenced by world events. Increased demand for U.S. produced LNG in Europe and Asia is resulting in higher natural gas costs for all consumers in the U.S.

Figure 1 – U.S. Liquefied Natural Gas Export Capacity by Project, U.S. Energy Information Administration (EIA)

Paradoxically, a continued expansion in LNG export capacity could benefit energy consumers in New England if it helps to moderate world LNG prices. New England is the only region of the U.S. that is heavily dependent on importing foreign natural gas to meet peak winter heating demand. To attract scarce wintertime LNG cargos, New England must compete with Europe and Asia on the world market. LNG prices in Europe and Asia are trading at more than $30 per MMBtu for the upcoming 12 months – six times the benchmark price of natural gas in the U.S. - due to concern that Europe’s supply of natural gas from Russia is at risk.

As a result, consumers in New England are facing some of the highest forward prices for natural gas in history for peak winter months. During the spring, summer, and fall, when heating demand is low, natural gas commodity prices in New England revert back to much more modest levels near the Henry Hub U.S. benchmark. Although New England only needs LNG shipments during the coldest winter months – prices for LNG (and oil) are currently high enough during these months that they significantly increase the annualized natural gas and electricity rates paid by most consumers. For consumers with high electricity or natural gas usage in the winter – e.g., those with high heating demands - the impact is proportionally greater, as these consumers use proportionately more of their gas demands on these same days.

New England’s unique reliance on LNG imports stems from insufficient natural gas pipeline import capacity to simultaneously serve regional heating demand as well as power generation demand on cold winter days. New natural gas pipeline import infrastructure will not be built for a variety of reasons, leaving the region dependent on liquefied natural gas import terminals near Boston and across the Canadian border in St. John’s, New Brunswick. Interestingly, New England cannot legally receive any domestic U.S. LNG cargos, even though the U.S. is one of the largest producers of LNG in the world and export facilities in Maryland and the Gulf Cost are nearby. Due to the 100-year-old Merchant Marine Act of 1920 (widely known as the Jones Act) LNG tankers are not allowed to move cargos between two U.S. ports unless they are U.S. built, flagged, and staffed – no significant LNG tankers in the world currently qualifies.

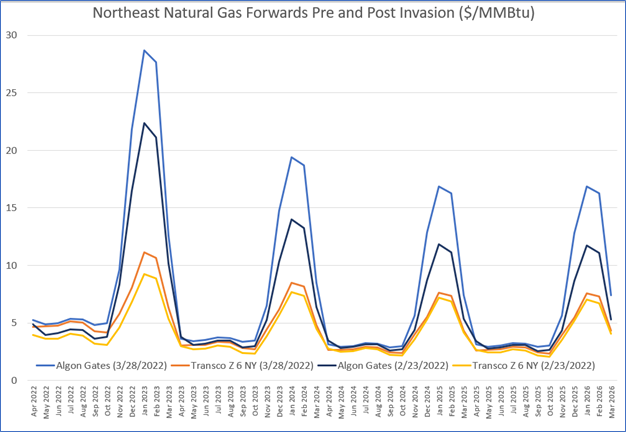

The following chart illustrates the price impact to New England consumers of the pre-existing winter natural gas pipeline capacity shortage as well as the impact of Russia’s invasion of Ukraine. The chart shows natural gas commodity prices along two pipeline systems: the Algonquin system within New England (light blue and dark blue) and the Transco system in New York (yellow and orange) for each future month between April 2022 and March 2026 on two different dates: 2/23/2022, the day before Russia invaded Ukraine, and 3/28/2022 the day this article was written. Comparing the yellow line and the dark blue line shows that New England was already seeing as much as a $13 per MMBtu premium compared to consumers in nearby New York, before the invasion. This premium reflects the lack of pipeline capacity to import enough natural gas into New England during peak winter months from the prolific Marcellus Shale in the Mid-Atlantic states. After the invasion, futures prices for both regions increased. Peak wintertime pricing increased $1 - $2 per MMBtu in New York and $5 - $6 per MMBtu next door in New England. As shown by comparing the orange line and the light blue line, New England pricing is as much as $17 per MMBtu higher than New York for the peak winter months of January and February 2023.

Figure 2 – Northeast Natural Gas Forwards Pre and Post Invasion ($/MMBtu). Graph by Competitive Energy Services, LLC.

Other U.S. electricity markets outside the Northeast are also impacted. Natural gas remains the marginal fuel for the generation of electricity for most hours in the majority of U.S. markets. As a result, the price that consumers pay for electricity is very closely linked with the price of natural gas and future electricity prices have increased along with forward natural gas pricing. As with natural gas, the price and volatility impacts for electricity are most severe in New England due to the region’s dependence on winter LNG imports.

The short-term consequences of Russia’s invasion of Ukraine on energy markets are very clear: higher prices and increased volatility for oil products, natural gas, and electricity. Longer term impacts are less certain.

A common saying among energy analysts is that “the solution to high prices is high prices.” High oil and natural gas pricing could result in a resurgence of the U.S. shale oil/gas industry that has shown uncharacteristic fiscal restraint after years of low prices caused by excess production capacity and the pandemic-induced collapse of demand. We are likely to see additional coal, natural gas, and oil production in the U.S., along with renewed interest in expanding energy export capacity as the U.S. seeks to bolster Europe’s ability to cut its reliance on Russian energy. The Biden administration recently pledged to significantly increase U.S. exports of LNG to Europe starting in 2022 and increasing through the end of the decade. The increased interest in coal, at least, will be transient as the fuel is incompatible with the decarbonization and health priorities of most major economies around the world. The interest in expanding U.S. oil and natural gas production, however, may be longer lasting. The majority of major international oil companies have announced that they will unwind activities in Russia. These companies may seek to redirect investments toward lower cost U.S. shale production. Combined with sanctions that limit Russia’s ability to access western capital markets, Russia’s technical capability to maintain its current levels of oil and natural gas production may diminish over time.

Even more influential than high energy prices, Russia’s invasion of Ukraine provided a stark reminder about the geopolitical risks of reliance on oil and gas. The desire for energy security has galvanized resolve in Europe and parts of the U.S. to accelerate the ongoing transition away from fossil fuels. All along the eastern U.S. seaboard, very large investments are being made in offshore wind power - a resource that will produce electricity most strongly during the winter heating season. Combined with the proliferation of air source and ground source heat pumps, intended to electrify, and decarbonize our winter heating needs, offshore wind will be a critical component of our future electric generation mix. Solar PV and electric vehicles are also being incentivized to reduce dependence on fossil fuels and lower carbon emissions.

Zero carbon energy projects, however, are not entirely immune to impacts from the war. Russia and Ukraine are both large producers of copper, nickel, platinum, aluminum, lithium, and uranium – all important inputs for solar, wind, batteries, and nuclear power systems. Delays and higher prices are already plaguing many clean energy projects across the U.S.

Western countries are moving with surprising speed and cohesion to reduce exposure to Russian energy. As the war in Ukraine drags on it becomes increasingly difficult to see this realignment of western countries away from Russian energy changing for decades to come. Russia will be able to mitigate the effects this realignment will have on its domestic energy sector by shifting energy exports east to China and India, thereby freeing up imports from the middle east to flow to Europe and resulting in a reshuffling of world energy flows instead of a net reduction.

The transition to an electrified and low carbon economy is complex. The realignment of worldwide energy sources and flows will take decades. Russia’s invasion of Ukraine has accelerated this transition somewhat, but it has also increased the turbulence that energy consumers will face along the way. Consumers across the U.S. will experience higher and more volatile pricing for most energy commodities because of the war in Ukraine. New England consumers will be more impacted than most. Eventually higher production of oil and natural gas from U.S. shale, the accelerating transition of western nations towards electrification and decarbonization and the redirection of Russia’s energy exports to the east will moderate longer term worldwide price impacts.

Photo by Javier Miranda